Bank Reconciliations: Steps, Examples, Best Practices

.png)

Every month, your accounting team needs to close the books. And every month, one task sits at the foundation of that process: bank reconciliation. It's how you confirm that your company's accounting records actually match what's sitting in your bank accounts.

When done right, bank reconciliation catches errors before they compound, spots fraudulent activity early, and gives your finance team confidence in the cash position they're reporting. This guide walks through the core steps, common pitfalls to avoid, and how modern accounting teams are using automation to turn what used to be a multi-day ordeal into a streamlined workflow.

Key Takeaways

- Bank reconciliation matches your accounting records against actual bank statements to ensure accuracy, detect fraud, and maintain confidence in your reported cash position.

- Reconciliation frequency should scale with risk, as high transaction volumes, regulatory requirements, or past control weaknesses warrant more frequent reconciliations beyond your standard month-end cycles.

- Comprehensive documentation is non-negotiable, with auditors expecting detailed records including preparer/reviewer sign-offs, reconciling items, and supporting evidence, with retention periods ranging from five to seven years depending on regulatory requirements.

- Automation eliminates manual reconciliation bottlenecks while strengthening controls through automated bank feeds, AI-powered matching, and built-in audit trails that support both speed and accuracy.

What is Bank Reconciliation?

Bank reconciliation is the process that helps you ensure your company's accounting records match your bank statements. It's a core account reconciliation and a way to double-check that the money you think you have matches what's in your company’s bank account. This process is crucial for performing accurate financial reporting and managing cash flow effectively.

Why Are Bank Reconciliations Important?

The bank reconciliation process plays a pivotal role in producing accurate financial statements as well as establishing solid cash flow management. By understanding and implementing bank reconciliation, you can keep polished financial records, detect any bookkeeping discrepancies, and ensure that your recorded cash balances are precise.

- Pinpointing Cash Flow: Bank reconciliation ensures you have a precise understanding of the money flowing in and out of your accounts. Knowing your exact cash position helps you make informed decisions, whether it’s paying a vendor or investing in new equipment. Without reconciliation, you might assume you have more or less money than you actually do, leading to poor financial decisions.

- Highlight Fraudulent Activity: Regular bank reconciliation helps detect discrepancies that may indicate fraud. For instance, if you notice a check amount that doesn’t match the recorded amount in your books, this could be a sign of tampering. By catching these issues early, you can take corrective actions before they escalate.

- Accounts Receivable Management: No one wants to leave money on the table, and unpaid invoices impact your entire order to cash process, which in turn affect your company revenue. Regular reconciliations help to spot invoices that haven’t been paid. Once identified, you can take steps to collect the payments, such as sending reminders or contacting the customer directly. Addressing these problems promptly ensures that your business maintains a healthy cash flow and reduces the risk of bad debts.

- Regulatory Compliance and Audit Readiness: Bank reconciliations create the documented audit trail that external auditors and regulatory bodies expect to see. Publicly traded companies face SOX compliance requirements, while organizations in regulated industries must prove they’re using robust financial controls. A consistent reconciliation process (with proper documentation and segregation of duties) satisfies these requirements and streamlines audit preparation.

- Investor and Stakeholder Confidence: Investors, lenders, and board members rely on accurate financial reporting to make decisions about your company. Regular bank reconciliations demonstrate financial discipline and control maturity, building the confidence that your reported cash balances and financial statements reflect reality rather than unverified book entries.

- Error Prevention and Correction: Reconciliation can go beyond catching fraud; it also surfaces honest mistakes before they cascade into larger problems. Whether it's a transposed digit, a duplicate payment, or a misclassified transaction, identifying errors during reconciliation prevents them from distorting month-end financials and creating confusion in subsequent periods.

- Risk Management: Bank reconciliations help you spot operational risks like unauthorized account access, check kiting schemes, or processing errors by your bank. Early identification of these issues allows you to implement corrective controls and prevent recurrence.

Types of Bank Reconciliation

Bank reconciliations can be classified into two main types: month-end and ongoing.

Month-end Bank Reconciliation

As a key part of the balance sheet reconciliation process, month-end bank reconciliations are performed at the end of each month to ensure that all bank transactions for the period are accounted for.

This process involves matching the bank statement with the company's general ledger account balance, identifying discrepancies, and making necessary adjustments. We’ll dive deeper into how to perform this recon below.

Ongoing Bank Reconciliation

Ongoing bank reconciliations are conducted more frequently, such as weekly or even daily, to maintain real-time accuracy in financial records. These reconciliations typically involve live transaction matching between an accounting system and a live feed from a financial institution, and reduce the risk of errors and fraud.

Reconciliation Frequency: Finding the Right Cadence

All finance teams ask the question: how often should I reconcile? The answer isn't one-size-fits-all. While monthly reconciliations align with standard accounting close cycles, many organizations benefit from increased frequency as they scale.

Monthly reconciliations work well for smaller organizations with predictable transaction volumes and strong controls. They align naturally with financial reporting periods, and provide sufficient oversight for low-risk accounts.

Weekly reconciliations suit mid-sized companies experiencing growth or managing moderate transaction volumes. This cadence catches errors before they accumulate, but still remains manageable for accounting teams.

Daily reconciliations become practical for high-volume environments, companies with significant fraud risk, or organizations in regulated industries. Treasury teams at larger organizations often reconcile cash-heavy accounts daily to maintain precise cash positioning.

Real-time or continuous reconciliation leverages automation to match transactions as they occur. This approach works best when supported by robust bank feeds and automated matching tools, turning reconciliation from a more periodic task into an ongoing monitoring process.

Risk-Based Assessment: Choosing Your Cadence

Your reconciliation frequency should reflect the risk profile of each account. Consider these factors when establishing your cadence:

- Transaction Volume: Accounts processing hundreds or thousands of transactions monthly warrant more frequent reconciliation. High volume increases error probability and makes investigation more difficult if problems accumulate over time.

- History of Fraud Incidents or Weaknesses in Control: If you've experienced unauthorized transactions, check tampering, or past control failures, you should increase reconciliation frequency for affected accounts until controls strengthen.

- Regulatory Requirements: Certain industries face mandated reconciliation frequencies. Trust accounts, broker-dealer cash accounts, and financial institutions often require daily reconciliation regardless of transaction volume.

- Cash Flow Volatility or Capital Constraints: When cash is tight or fluctuates significantly, frequent reconciliation provides the visibility needed for informed cash management decisions. Organizations managing covenant compliance or facing liquidity challenges benefit from daily cash position updates.

Modern bank reconciliation automation tools like Numeric’s Cash Management eliminate the manual burden that traditionally made frequent reconciliation impractical. Automated bank feeds, AI-powered transaction matching, and exception-based workflows allow teams to increase reconciliation frequency without proportionally increasing headcount. This shift ultimately strengthens controls while improving cash visibility.

How to Do Bank Reconciliation: 5 Key Steps

Step 1: Compare Balances

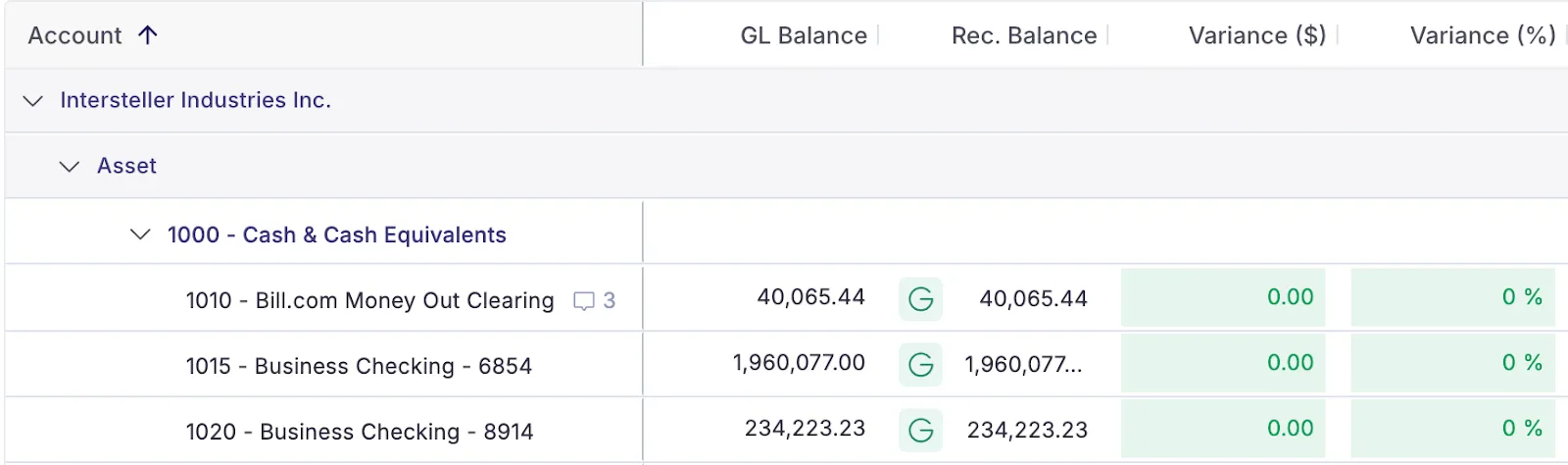

Start by aligning the bank account balance with the cash balance on your company’s balance sheet. Put both your bank statement and your cash balance side by side. Keep in mind that the balances will rarely match exactly, so don't be alarmed if this is the case.

If using Numeric, AI will scan and pull the balance from any uploaded bank statements to compare directly against the GL total. These balances sit side-by-side in your auto-generated reconciliation report each month.

Step 2: Review Bank Statement

Next, dive into your bank statement to find transactions that aren’t yet reflected in your company’s books. Look for items such as bank fees, wire transfer fees, and interest income. These transactions might not have been recorded in your books yet because they occurred after your last update. Note these discrepancies for the next steps.

When discrepancies happen, these investigative approaches can help you get to the bottom of them:

- Transposition error check: If the difference between balances is divisible by 9, you likely have a transposition error (e.g., recording $1,234 as $1,243). Review recent entries for reversed digits.

- Duplicate entry detection: Sort transactions by amount and date to quickly spot identical entries posted multiple times. Duplicate payments or deposits are common culprits when balances don't reconcile.

- Timing difference analysis: Separate transactions by those that should have cleared versus those still in process. Outstanding checks and deposits in transit explain many reconciliation differences without indicating errors.

- Missing transaction search: Compare your GL transaction list against the bank statement line by line for the period. Missing entries—whether bank fees you forgot to record or deposits that never hit the bank—will surface through systematic comparison.

Step 3: Review Account Trial Balance

Now, turn your attention to your recorded cash balance and identify transactions recorded in your books that don't appear on your bank statement. Two common examples are:

- Outstanding Checks: these are checks you've issued but the recipients haven't cashed yet

- Deposits in Transit: these are deposits you've recorded in your books but haven't yet been processed by the bank.

Make a list of these items as they will need to be accounted for to reconcile the balances.

Numeric's deep NetSuite integration gives teams access to transaction-level details across their accounts.This makes bank recons easier, as you can pull up and pivot transactions directly in the Numeric platform.

Automate your bank reconciliations with Numeric’s #1 Cash Management tool

.png)

Step 4: Adjust Balances

Once you’ve identified the discrepancies, make any necessary adjustments. This step ensures your records accurately reflect your financial status.

- Adjust GL Bank Account Balance: Adjust the bank account balance for outstanding transactions identified in the previous step. Calculate how the balance will change once these transactions are processed. For example, if there are $5,000 in outstanding checks, subtract this amount from the bank balance. If there are $2,000 in deposits in transit, add it to the bank balance.

- Adjust Book Balance: Add or subtract bank transactions that haven’t been recorded in your books but appear on your bank statement. For instance, if there is a $50 bank fee, subtract it from your book balance.

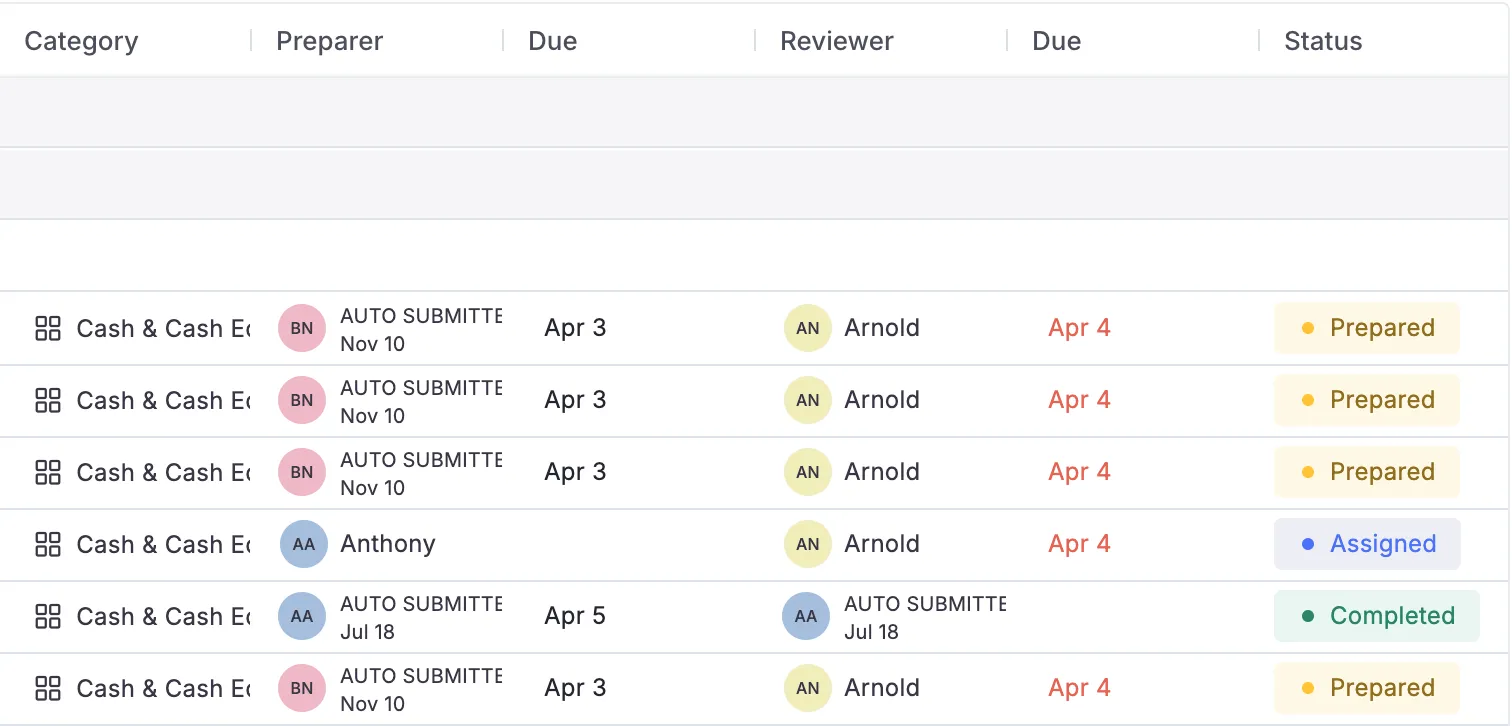

Step 5: Record the Reconciliation

Finally, document the entire reconciliation process, at a minimum capturing who prepared and reviewed the reconciliation and when. This statement should itemize every discrepancy, showing the date, amount, and reason for each adjustment. Proper documentation ensures that you maintain a clear record for future reference and auditing purposes.

Comprehensive documentation serves multiple purposes, including creating an audit trail, maintaining and proving regulatory compliance, and offering fraud investigation support. Your reconciliation documentation is the evidence that your controls actually function as designed.

Required documentation elements include:

- Date of reconciliation and period covered

- Preparer name and signature

- Reviewer name and signature (separation of duties)

- Beginning and ending balances (bank and book)

- Complete list of reconciling items with descriptions

- Supporting evidence for all adjustments (bank statements, deposit slips, voided check copies)

- Explanation of unusual or material items

- Resolution status of outstanding items from prior periods

Document Retention Compliance

How long should you retain bank reconciliation records? The answer depends on your regulatory requirements:

- GAAP: Minimum seven years for publicly traded companies

- State requirements: Often five to seven years for trust accounts, but this varies by state

- IRS: Seven years for tax-related documentation

- PCAOB AS 1215: Specific retention and documentation standards for audit work papers (effective December 15, 2026)

As a result, modern best practice favors digital documentation with:

- Automated audit trails showing who accessed or modified records

- Cloud storage with redundant backups

- Version control for amended reconciliations

- Integration with general ledger systems for seamless journal entry posting

Digital documentation makes audit preparation faster and reduces the risk of lost or misfiled paper records.

Numeric eliminates the busywork from documentation by automatically recording when a reconciliation has been reviewed and completed, along with any associated comments.

Real-World Example for Reconciling Bank Statements

John Franklin is a staff accountant for the computer hardware company, ABC Widgets, who has been tasked with reconciling the company’s cash accounts for month-end.

When he receives the bank statement for one of the business accounts, a checking account, he sees that it has an ending balance of $9,800 while the company’s book balance shows $10,500.

Here’s how John can reconcile these differences.

- Compare Balances: In looking at the trial balance for the bank account and the bank statement balance, John sees that there is a difference of $700.

- Review Bank Records: When John checks the bank statement, he sees that the account accrued $50 in interest earned and that the bank issued a service fee of $300. While these charges are documented in the statement, they aren’t reflected in the books.

- Review Book Records: John looks into the company’s records to initially check for two things: outstanding checks and deposits in transit. some text

- Identify Outstanding Checks: John first checks to see if checks have been recorded in the books but not yet cleared by the bank. He sees two outstanding checks: Check #201 for $300 and Check #223 for $150. They amount to $450.

- Locate Deposits in Transit: John sees that ABC Widgets made a deposit of $900 on the last day of the month, which hasn’t cleared yet.

- Adjust Balances: To remediate these discrepancies, John makes adjustments to each balance, including:

- GL Balance: He adds the $900 of deposits in transit and subtracts the $450 of outstanding checks from the general ledger balance of $9,800 to arrive at an adjusted bank balance of $10,250.

- Trial Balance: He subtracts the $300 of bank fees and adds the $50 of interest earned to the book balance of $10,500 to arrive at an adjusted book balance of $10,250.

- Record the Reconciliation: After completing the adjustments, John creates a bank reconciliation statement listing all balances before and after the reconciliation, as well as all updated journal entries. By doing this, he ensures that the financial records are up-to-date and will align appropriately with the next period’s reconciliation.

Common Challenges with Bank Reconciliation

Even experienced accounting teams face recurring obstacles during bank reconciliation. Understanding these challenges and implementing prevention strategies can transform reconciliation from a monthly headache into a controlled, efficient process.

Data Entry Errors

Data entry mistakes are among the most common reconciliation challenges. A single transposed digit or duplicate entry can throw off your entire reconciliation and consume hours of investigation time.

Examples: Transposed numbers ($1,234 entered as $1,243), duplicate entries, missing transactions, incorrect amounts

Prevention Strategies:

- Implement validation rules in accounting software

- Use automated bank feeds instead of manual entry

- Require dual entry for transactions above materiality threshold

- Enable real-time data validation alerts

Misclassification Errors

Even when transaction amounts are correct, posting to the wrong account creates reconciliation problems and distorts financial reporting across your chart of accounts.

Examples: Posting to wrong accounts, incorrect expense categories, misallocated customer payments

Prevention Strategies:

- Standardize chart of accounts with clear descriptions

- Provide regular training on classification rules

- Implement approval workflows for unusual transactions

- Use automated matching rules for recurring transactions

Timing Differences

Not all reconciliation differences indicate errors, and legitimate timing differences that require tracking rather than correction.

Examples: Outstanding checks, deposits in transit, in-process transactions

Prevention Strategies:

- Maintain detailed outstanding check registers with aging analysis

- Investigate checks outstanding >90 days (may require stop payment and reissuance)

- Track deposits in transit separately; investigate if not cleared within 3 business days

- Reconcile more frequently to minimize timing difference accumulation

Documentation Deficiencies

Missing or inadequate documentation makes reconciliation investigation difficult and creates audit findings. Without proper supporting evidence, you can't explain or verify adjustments.

Examples: Missing receipts, unclear transaction descriptions, inadequate supporting evidence

Prevention Strategies:

- Implement mandatory documentation policies (no posting without support)

- Use digital receipt capture tools (mobile apps, email forwarding)

- Require detailed descriptions at point of entry

- Create standardized naming conventions for recurring transactions

Software and System Issues

Technology should streamline reconciliation, but system failures, integration problems, and data synchronization errors can create new challenges when not properly managed.

Examples: Bank feed import failures, synchronization errors between systems, software version incompatibilities, corrupted data files

Prevention Strategies:

- Perform regular system testing and updates

- Maintain backup procedures for manual import if feeds fail

- Document integration points and troubleshooting procedures

- Implement data validation checks after imports

Review Process Failures

Even perfect reconciliation preparation fails if review procedures are inadequate. Rubber-stamp approvals, lack of segregation of duties, and insufficient investigation of discrepancies undermine control effectiveness.

Examples: Lack of oversight, no separation of duties, inadequate investigation of discrepancies, rubber-stamp approvals

Prevention Strategies:

- Establish formal review procedures with documented sign-off

- Rotate reconciliation responsibilities periodically

- Define materiality thresholds requiring escalation

- Implement surprise audits of reconciliation quality

Best Practices for Bank Reconciliation

Strong bank reconciliation processes share common characteristics: consistency, control, and attention to detail. These practices help accounting teams maintain accuracy while improving efficiency.

Building a resilient reconciliation process requires more than just following steps—it demands intentional design of workflows, controls, and quality standards that scale with your organization.

Performing Reconciliations on a Set Schedule

Consistency is key, and regular reconciliations prevent discrepancies from accumulating.

Aim to reconcile your bank statement at least once a month. Some businesses, particularly those with high-volume financial transactions, may benefit from weekly or even daily ongoing reconciliations to ensure any errors or fraudulent activities are caught early.

Leveraging Technology for Automation

Automation can significantly streamline bank reconciliation by cutting down on time-consuming manual tasks and minimizing errors.

For teams looking to move away from a manual reconciliation process and towards finance process automation, close automation accounting software is key.

Since Numeric can automatically pull a company’s trial balance and totals from bank statements, teams automate much of the reconciliation process and can auto-submit recons that are below the materiality threshold.

Detailed Documentation

It’s imperative to maintain detailed sets of records of the current reconciliation process and any adjustments made. Proper documentation is vital for transparency and accountability.

Each step of the reconciliation process should be clearly recorded, including any discrepancies found and the actions taken to resolve them. This practice not only aids in internal reviews but also provides an audit trail.

Implement Segregation of Duties

Never allow the same person to prepare and approve their own reconciliations. Segregation of duties is a fundamental internal control that prevents fraud and catches errors through independent review.

The person reconciling the account should be different from those who process transactions or have check-signing authority. This separation creates natural checkpoints that strengthen your overall control environment.

Establish Materiality Thresholds and Investigation Protocols

Not all reconciliation differences warrant the same level of scrutiny. Define clear materiality thresholds that determine when differences require investigation versus when they can be written off or carried forward.

For example, differences under $100 might be investigated only if they appear repeatedly, while variances over $10,000 demand immediate explanation and resolution.

Document these protocols so your team applies consistent judgment across all reconciliations.

Document and Review Reconciliation Quality

Beyond documenting the reconciliation itself, track metrics that indicate process health: average time to complete, number of reconciling items, aging of outstanding items, and frequency of errors discovered.

Periodic quality reviews—whether by internal audit, Controllers, or external firms—identify process weaknesses before they become audit findings. Use these insights to continuously refine your approach.

Prepare for Audits Proactively

Don't wait until audit season to organize your reconciliation documentation. Design your process with audit requirements in mind from the start:

- Maintain organized digital files with clear naming conventions.

- Ensure all reconciliations include proper sign-offs and supporting documentation.

- Track resolution of outstanding items from period to period.

When auditors request bank reconciliations, you should be able to provide complete, well-documented evidence within minutes, not days.

Advanced Reconciliation Scenarios

As organizations scale, reconciliations can become more complex. What works for a single-entity company with one bank account breaks down when you're managing multiple subsidiaries, currencies, or thousands of daily transactions. Here's how to approach increasingly sophisticated reconciliation scenarios.

High-Volume Transaction Environments

Companies processing hundreds or thousands of transactions daily face unique challenges. Manual reconciliation becomes impractical, and even small error rates create significant investigation burdens.

Follow these steps:

- Implement automated matching rules that handle routine transactions (payroll, recurring vendor payments, subscription revenue) without manual intervention.

- Focus human review on exceptions and transactions that fall outside normal patterns.

- Consider real-time reconciliation tools that flag discrepancies as they occur rather than discovering them weeks later.

- Set statistical thresholds. For example, auto-match transactions under $500 that match on amount and date, but flag larger items for manual review.

Multi-Currency Reconciliation

Organizations operating globally must reconcile accounts denominated in multiple currencies, introducing foreign exchange gains and losses that complicate the matching process.

Here’s what to keep in mind:

- Reconcile foreign currency accounts in both the original currency and your reporting currency.

- Track exchange rate variances separately from operational differences, as commingling these creates confusion and makes root cause analysis difficult.

- Use your ERP's functional currency conversion features rather than manual calculations to ensure consistency.

- Consider reconciling foreign accounts more frequently since exchange rate volatility can make month-old outstanding items difficult to validate.

Subsidiary and Intercompany Reconciliation

Multi-entity organizations must reconcile not just bank accounts but also intercompany transactions to ensure subsidiary books tie to consolidated financials.

Here’s what to do:

- Establish strict intercompany policies requiring both sides of each transaction to record entries using matching reference numbers and amounts.

- Reconcile intercompany accounts monthly at minimum, since letting these drift creates consolidation nightmares at quarter and year-end.

- Implement automated intercompany matching tools that flag one-sided entries or amount mismatches in real-time.

- Designate clear ownership for resolving intercompany discrepancies rather than allowing them to languish unresolved.

Real-Time and Continuous Reconciliation

Leading organizations are moving beyond periodic reconciliation toward continuous monitoring that identifies and resolves discrepancies daily or even in real-time.

Continuous reconciliation requires robust system integration, as your accounting platform must sync with bank feeds automatically and frequently. Here’s how to get started:

- Start with high-volume, high-risk accounts before expanding to all bank accounts.

- Define exception workflows that route unmatched transactions to appropriate team members for resolution.

- Monitor aging of outstanding items daily and escalate those that remain unresolved beyond defined timeframes.

Real-time reconciliation shifts the focus from period-end scrambling to ongoing maintenance, dramatically reducing month-end close time.

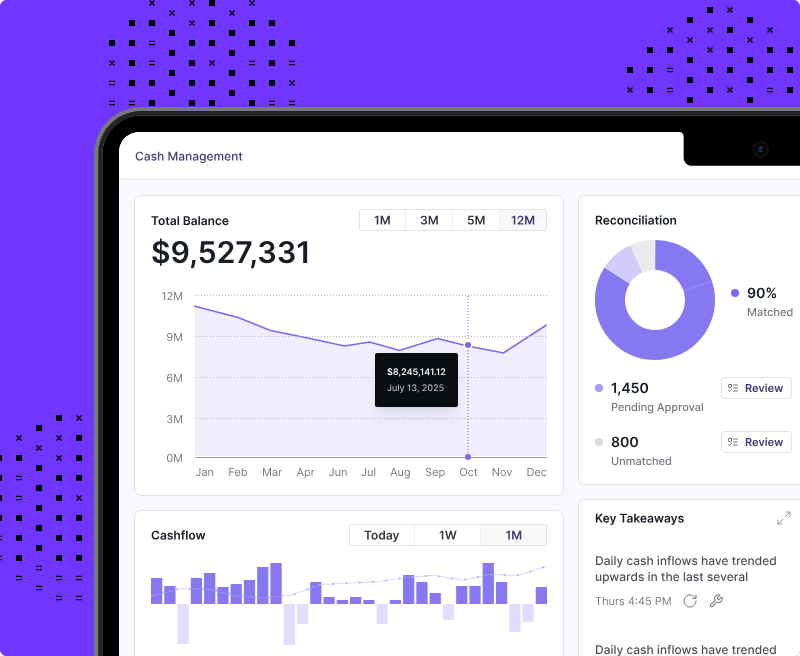

How Numeric Helps Accounting Teams with Bank Reconciliation

Numeric's Cash Management and Cash Matching products automate 90%+ of bank reconciliations through AI-powered transaction matching and real-time NetSuite integration.

Key capabilities include:

- Flexible rules engine: Handles all match types (1-to-1, 1-to-many, many-to-many) without complex Excel formulas

- Real-time GL sync: Pulls live transaction data from NetSuite for continuous reconciliation

- Direct posting to NetSuite: Draft and batch-post hundreds of journal entries in a single click

- Centralized exception handling: Surface unmatched transactions and resolve issues in one workspace

- Audit-ready documentation: Built-in logging, approval workflows, and support linking for compliance

Numeric enables teams to move from month-end fire drills to continuous, controlled reconciliation. Real-time visibility and proactive monitoring catch issues early, reducing stress and improving accuracy.

Numeric is purpose-built for NetSuite users, with deep integration and native support for multi-entity, multi-currency, and complex organizational structures. Schedule a demo to see how Numeric can transform your bank reconciliation process.

The Bottom Line on Bank Reconciliation

Ultimately, bank reconciliation is a relatively straightforward accounting process that is essential for understanding a company’s cash position. Companies that stay on top of bank reconciliation not only keep their accounts in check but can also strengthen their overall financial strategy.

Frequently Asked Questions (FAQ)

Related Content

The Finance Engineer: Why Accountants Are the Best Builders in the Room

Why accountants, not engineers, are becoming the best builders on modern finance teams. Meet the Finance Engineer.

.png)

Numeric vs. Ledge: What's the Best Close Platform for Your Business?

A detailed comparison of Numeric and Ledge, two modern close management platforms, covering features, architecture, pricing, and a framework for choosing the right fit for your team.

.png)

What is Record to Report: Process, Steps, and Benefits

Learn how the Record to Report process works, from transaction capture to financial reporting. Discover steps, challenges, automation strategies, and best practices for modern accounting teams.