A Controller's Guide to Construction-in-Progress (CIP) Accounting

.webp)

Every construction project tells a story – one that sees the power of human creativity turn nuts, planks, & bolts into impressive tools and structures. However, teams that forget to correctly account for those fixed assets, their usage, etc. will quickly see the financial side of that story spin into a mystery novel.

CIP – construction-in-progress – accounting isn’t just another box to check on the way to having new silos and sheds. It’s the bridge between budgets, blueprints, and the assets that eventually hit your balance sheet. If your projects could talk, would they tell a clear, consistent financial story? Or would they leave your leadership team asking questions you’d rather not answer?

Strong CIP management is just about tracking costs – it’s about giving your business the visibility it needs to plan with confidence.

This guide explains the essential principles of CIP accounting and provides practical strategies for Controllers to maintain accuracy, compliance, and financial clarity throughout your construction projects.

Essential CIP Journal Entries and Accounting Treatment

Precise journal entries are fundamental to effective CIP accounting. The following examples illustrate standard transactions throughout a construction project lifecycle, ensuring costs are properly recorded in compliance with accounting standards.

Recording Initial Project Costs

When materials arrive for a CIP project, proper allocation to the specific project account is essential:

Debit: CIP – Project A $50,000

Credit: Accounts Payable $50,000

This entry records the liability for materials purchased while allocating the cost directly to the appropriate CIP account.

Capturing Labor and Overhead

Labor and allocated overhead directly contributing to construction should augment the CIP debit balance:

Debit: CIP – Project A $75,000

Credit: Payroll Expenses Payable $60,000

Credit: Overhead Allocation $15,000

This transaction captures both direct labor and appropriate overhead costs that qualify for capitalization under accounting standards.

Handling Borrowing Costs

Under IFRS, borrowing costs directly attributable to qualifying assets must be capitalized:

Debit: CIP – Project A $10,000

Credit: Interest Payable $10,000

This entry reflects interest on construction financing in accordance with IAS 23 requirements.

Addressing Scope Changes

When project modifications require abandonment of previously capitalized components:

Debit: Expense – Abandoned Project Costs $5,000

Credit: CIP – Project A $5,000

This adjustment reclassifies costs for eliminated project elements as current expenses, maintaining CIP accuracy.

Completing the Project

Upon project completion, the accumulated CIP balance transfers to the appropriate fixed asset account:

Debit: Building – Headquarters $1,000,000

Credit: CIP – Project A $1,000,000

This entry clears the CIP account and establishes the fixed asset basis for future fixed asset depreciation.

These journal entries provide the accounting framework to properly track construction costs from initial expenditure through project completion, ensuring accurate financial reporting throughout the asset development cycle.

Understanding CIP vs. WIP: Critical Distinctions

Construction-in-Progress (CIP) and Work-in-Progress (WIP) accounting share similar terminology but serve fundamentally different accounting purposes.

When to Use CIP

CIP accounting is used for long-term capital assets under construction or development that will eventually appear on the balance sheet as fixed assets. These projects represent significant investments in physical infrastructure, facilities, or major equipment installations.

When to Use WIP

WIP accounting, conversely, applies to inventory production where goods remain incomplete. These partially finished goods represent inventory rather than fixed assets. WIP includes materials, direct labor, and allocated overhead for products still moving through production.

Financial Statement Impact of CIP and WIP

How CIP and WIP show up on key financial statements differs as well.

- Balance Sheet: CIP appears as a fixed asset account under the non-current assets section, while WIP generally is included in inventory as a current asset.

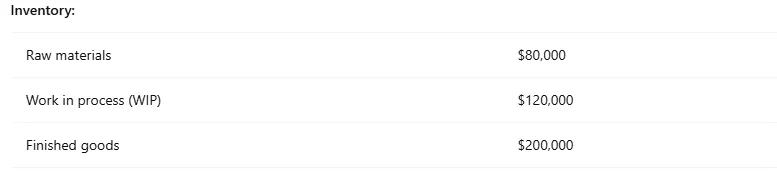

Large WIP balances can be presented as separate line items, as shown below.

- Income Statement: CIP costs remain on the balance sheet until project completion, whereafter they move to fixed assets and begin depreciation. WIP costs eventually flow to COGS (Cost of Goods Sold) on the income statement once finished goods are sold.

Key Steps for Managing CIP Accounting

Whether your company is constructing a new warehouse or developing new software, use these tips in your accounting process to make your CIP accounting manageable.

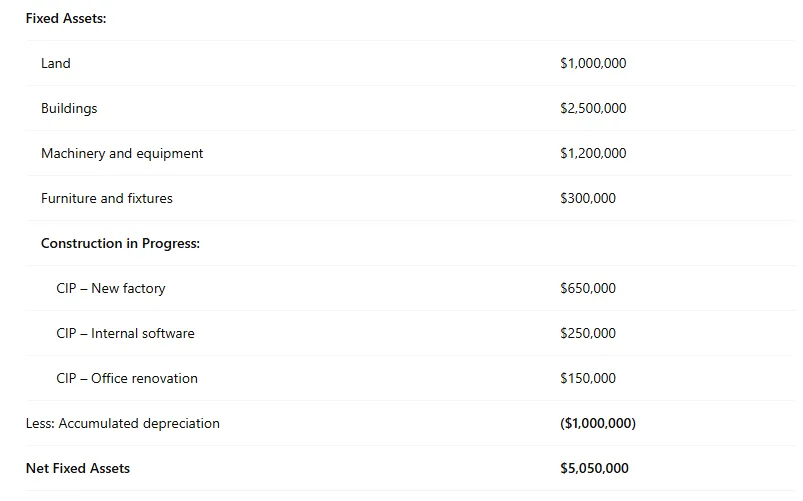

1. Create Unique CIP Accounts

Each construction or development project should have its own CIP general ledger account in your fixed asset/long-term asset section of the balance sheet. For improved transparency and financial analysis, don’t lump all CIP costs into one general ledger account.

Alt text: A balance sheet showing construction-in-progress accounts for a new factory, internal software, and office renovations listed individually under the fixed assets section.

2. Begin Cost Tracking

Comprehensive record-keeping forms the backbone of successful CIP accounting. Without it, you may miss expenses or misallocate costs, which can undermine project budgets and financial reporting accuracy.

If your primary accounting software lacks detailed project accounting functionality, supplemental tools with dedicated checklists, audit trail, and other project management features can help capture all your cost data.

Preventing overlooked costs and other discrepancies begins with diligent cost tracking. Regular reviews of expense reports, vendor invoices, and project documentation all help in identifying missing items before they affect financial statements. Cross-functional coordination between accounting, procurement, and project management teams further strengthens your control environment.

3. Account for Scope Changes

Scope changes require special attention in CIP accounting. Modifications to project scope or design in the construction phase present significant accounting challenges.

These adjustments—ranging from design alterations to material upgrades or regulatory accommodations—may increase overall costs, create new cost classification requirements, or cause write-offs of previously capitalized expenses.

When project scope changes, previously capitalized costs require scrutiny. Expenses already recorded in CIP accounts may no longer qualify for capitalization if they relate to abandoned or substantially altered portions of the project.

For instance, assume a partially completed warehouse no longer meets regulatory safety requirements. All the costs to build the partial warehouse must be removed from CIP and immediately expensed, and the related demolition costs are also expensed.

Key considerations when managing scope changes include:

- New Cost Evaluation: Assess whether additional costs resulting from scope changes meet capitalization criteria under applicable accounting standards. Document the rationale for inclusion or exclusion from CIP accounts.

- Write-Off Procedures: For abandoned project components, remove associated costs from CIP and recognize appropriate write-offs to reflect the financial impact.

Extensive documentation for scope changes is necessary to withstand audit scrutiny, especially when they involve significant write-offs or substantial cost increases. Maintaining records—including change orders, revised budgets, and updated project specifications—provides the evidence needed to substantiate accounting decisions and show compliance with applicable standards.

4. Record Capitalizable Costs

Throughout the construction process while you’re tracking all expenses, you’ll need to evaluate which expenses need to be capitalized.

(While ASC 360-10-05-3 defines what property, plant, and equipment are, it doesn’t include specifics on capitalizable costs. Instead, you’ll likely need to refer to secondary sources discussed in this comprehensive PP&E guide published by PWC.)

In short, only costs directly attributable to bringing the asset to its working condition are recorded in CIP accounts. For example, preliminary assessments, speculative planning, fines and penalties, or post-completion enhancements rarely qualify for capitalization and should be expensed as incurred.

Download Numeric’s Fixed Asset Workpaper

For teams looking for streamlined fixed asset management, this fixed asset workpaper provides all the necessary components.

Numeric: where audit readiness awaits

.png)

Tackling Common CIP Accounting Challenges

Unlike traditional inventory or fixed asset tracking, CIP often involves more judgment, cross-department collaboration, and long timelines, opening the door for missteps.

Completed Projects Sit in CIP Too Long

Of all the issues related to CIP accounting, this one tends to be the most frequent. A project is completed, but crickets…no one told the accounting team. As a result,

- The asset isn’t depreciated when it should be

- The financial statements overstate CIP and understate fixed assets

- Budget-to-actual capital spend reports are thrown off

As such, it’s best for teams to establish a clear handoff process between the project manager and the accounting team. When the project hits substantial completion, accounting should receive a formal notice that includes the date and details of any additional expenses to get the project to a final completion.

Poor Cross Departmental Communication

CIP accounting, much like any other form of accounting, requires coordination across multiple departments in a company. Along with causing capitalization and depreciation delays, failed communication creates challenges like:

- Computer systems for project management and accounting aren't integrated

- Technical and financial perspectives on project completion differ

- Responsibility transitions during long projects, creating confusion about who’s currently overseeing the project

Instead, ditch the department silos by creating a cross-functional CIP "war room" that brings the finance department, project teams, and operations together for quick-hit monthly reviews of active projects. Or, for continuous real-time visibility, implement a digital dashboard with automated alerts when projects hit critical milestones or exceed thresholds.

Missing Supporting Documentation

What accountant doesn’t love their supporting documents? Invoices. Purchase Orders. Timesheets. They’re all necessary for accurate CIP accounting.

Best Practices for Consistent CIP Excellence

Make budget overruns and overdue cost analysis a thing of the past when you follow these best practices for your CIP accounting.

Audit Preparation and Documentation

Regular audits, both internal and external, provide assurance of CIP account accuracy, compliance, and financial reporting integrity. Because of their complexity and materiality, CIP accounts typically receive heightened scrutiny during audit engagements.

Effective audit preparation includes:

- Scheduled Reviews: Implement quarterly internal audit reviews to verify CIP balances against project milestones. Consider planning comprehensive annual external audits for independent assessment of CIP practices.

- Documentation Readiness: Recognize that significant capital investments attract audit attention due to their materiality and the judgment needed for cost capitalization. Be prepared with all your documentation in order.

- Verification Procedures: Ensure auditors can easily trace costs from general ledger entries to supporting documentation, including invoices and contracts. Reconcile CIP balances with project status reports to confirm correct capitalization treatment.

- Control Environment: Establish clear controls including capital expenditure approvals, regular reconciliations, and appropriate authorization levels to prevent misstatements before they impact financial reporting.

- Audit Readiness Checklist: Develop a standardized preparation list including required documentation, reconciliations, and project timelines. Designate primary contacts for auditor communication to streamline complex transaction explanations.

Well-designed controls and thorough audit preparation not only reduce errors, but also build stakeholder confidence in accurate financial reporting and management effectiveness.

Developing Team Expertise

A well-trained accounting team forms the foundation of effective CIP management. The complexities of tracking capitalized costs, handling scope changes, and applying accounting standards demand both technical knowledge and current regulatory awareness. Investing in team education provides the confidence and capability to address CIP complexities.

Maintaining Transparency and Compliance

Adherence to accounting standards while maintaining transparent CIP practices builds stakeholder trust. Clear, consistent reporting of CIP activities enables better financial management based on reliable financial information.

Bottom Line

Strong CIP accounting is a necessity for accounting teams in the farming, transportation, or construction industries. By practicing appropriate CIP treatments, teams create a real-time, audit-ready financial command center for capital projects.While this guide covered key principles and pitfalls, one often overlooked opportunity is using CIP data to forecast depreciation and future maintenance costs. By projecting these expenses early, you can better plan budgets, allocate resources, and align capital investments with long-term financial strategy and cash flow.Getting CIP right means fewer surprises at audit time and financial foresight for better strategic decisions all year long.

Related Content

Numeric Hosts The First Finance Engineer Cup

Four accountants built real AI tools for their own close and competed live. See how Alexandria Ramirez won Numeric's first Finance Engineer Cup.

The Finance Engineer: Why Accountants Are the Best Builders in the Room

Why accountants, not engineers, are becoming the best builders on modern finance teams. Meet the Finance Engineer.

.png)

Numeric vs. Ledge: What's the Best Close Platform for Your Business?

A detailed comparison of Numeric and Ledge, two modern close management platforms, covering features, architecture, pricing, and a framework for choosing the right fit for your team.