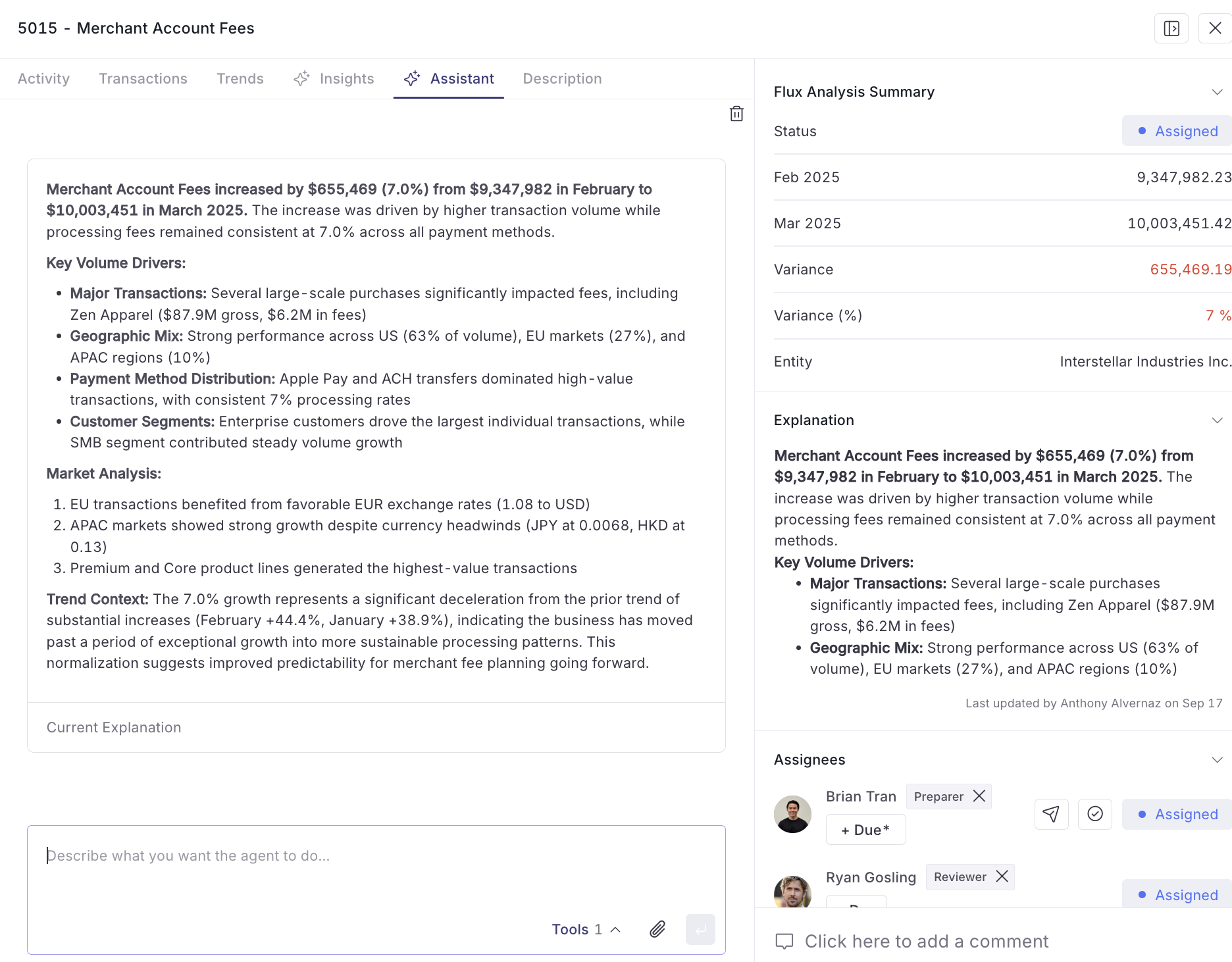

The Financial Close Process: A Complete Guide for Modern Teams

.png)

The financial close is your team’s opportunity to close the books on a specific time horizon. Month-end, quarter-end, and year-end closes are exactly what they sound like: processes to finalize all accounting records for the period in question.

The close is key because it provides the basis for decision-making across your organization. Without the close, accountants wouldn’t issue regular reports. Executives wouldn’t conduct periodic reviews, managers wouldn’t have data upon which to base forecasts, and investors wouldn’t receive updates on performance.

The financial close gives everyone a chance to sync up. But to have real impact, the close must be accurate and insightful, and you must deliver it without delay. This is easier said than done; around half of finance teams today complete the month-end close in 6 days or more.

A slow close means a slowdown in the data and analysis that decision-makers depend on. A fast close, on the other hand, opens the door to swift and decisive management actions.

This guide will help you understand the financial close at a granular level, along with its process components, common pain points, and modern best practices. Let’s close.

Key Takeaways:

- The financial close is essential for decision-making. Modern teams cut cycles from 10+ to 3–5 days through automation and integration.

- Continuous close practices keep books audit-ready and free time for analysis.

- Automation accelerates reconciliations, accruals, and reporting while improving accuracy and visibility.

- Clear governance via close calendars, RACIs, and checklists ensures accountability and consistency.

- AI enhances the close with anomaly detection, variance explanations, and automated report generation, but doesn’t replace your accounting team’s judgment

With Numeric, you can automate the close, ensure audit readiness, and give your accountants time back to focus on strategically important work

What is the Financial Close Process?

The financial close is a process undertaken by your organization’s finance team to finalize and “close out” the accounting records for a given time period.

Typically, the shortest time interval requiring a formal close is one month, corresponding to the “month-end close”. Quarter-end and year-end closes are also standard practice. Note that closes can be consolidated; if your fiscal year ends in December, for instance, the December close (which takes place at the beginning of January) will be a month-end, quarter end, and year-end all rolled into one.

Each close looks back on its respective period (whether that’s a month, a quarter, or a year) in order to give stakeholders a clear view of performance. From the CEO to department heads and profit center leaders, decision-makers at every level of your organization need a common dataset to reach consensus on how to steer strategy. For this, look no further than the financial close.

Historically, the close has been a slow and stressful process. Numeric gathered research on close timelines last year, and found that in 2022, 54% of teams were delivering a quarter-end close in 7 or more business days. In 2017, month-end closes took the median team about 6 business days.

Depending on timing, 6 or 7 business days can amount to almost half a month. By that time, the data being presented isn’t as timely, which undermines the confidence of any subsequent decisions.

Accounting technology has come a long way since then. The modern approach to the financial close condenses cycle time, thereby improving the reliability of data and analysis.

The Traditional Close vs. the Modern Close

The financial close has always played a crucial role in accounting. It produces the data and financial statements that the entire organization relies on, but it’s also essential for meeting compliance and reporting requirements.

So, there’s no getting around the need for a close at the end of each period. Teams can make the process easier, however, through incremental improvements to speed, accuracy, and strategic value.

The table below summarizes aspects of the financial close, with a comparison between traditional and modern approaches for each.

Taken altogether, there’s clearly a wide gap between a fully traditional and a fully modern close.

The key difference is that a modern close relies on integration, automation, and centralized processes. The traditional close, meanwhile, is made up of disconnected systems which require manual effort to reconcile and coordinate.

Manual Close Processes = High Costs

A considerable amount of manual work is required to execute a traditional financial close.

Among the specific tasks which occupy a team’s time during the financial close process, some are more daunting than others. Account reconciliation, accruals and provisions, and data hygiene were cited as the most time-consuming tasks in a recent survey. This suggests that when data is in different places, it becomes the responsibility of accountants to locate it, bring it back to one place, and make sure it looks right. Only then can the laborious process of reconciliation begin.

When this entire workflow is manual, it’s no surprise that accountants dread the financial close.

A slow close harms your organization, but there are individual costs, too. In a 2022 study, 81% of accounting and controlling professionals said the monthly financial close disrupted their personal lives. Employee burnout and retention can ensue from overly manual workflows, and it can create a vicious cycle: when team members don’t have the bandwidth to do strategic work, they’re less invested in the organization’s outcomes, which leaves them less motivated to fix issues and improve workflows.

That’s why leadership is ultimately responsible for modernization. Investing in effective tools, developing better workflows, and setting the table for success begins at the top.

The Strategic Value of a Modern, Optimized Close

Any organization can benefit from modernizing their financial close. Having up-to-date data is upstream of benefits like more agile planning, improved forecast accuracy, reduced audit and compliance risk, and superior liquidity management.

These are potential competitive advantages. However, a modern close also creates internal benefits. Liberating finance team members from the endless manual work of a traditional close gives them more time to dedicate to impactful analysis. They’ll be happier and less likely to churn as a result, but they’ll also be in a position to act as business partners across the organization, advising on strategic planning and democratizing access to financial data.

Many of these benefits go hand-in-hand. Modernizing your financial close process can lead to gains in efficiency, speed, and strategic value through higher-quality data and more effective accountants.

So, with the opportunity clearly defined, the next question is how best to execute.

Core Components of the Financial Close Process (And How to Modernize Them)

To successfully close out the books at the end of a month, quarter, or year, finance teams must manage several components of the process at the same time. These components build on one another, so they all contribute to a satisfactory and speedy close.

Here’s a summary of each component, along with the approach that modern teams are using.

Transaction Processing and Cutoff

Transaction processing isn’t just part of the financial close. It’s an ongoing practice which involves recording, reviewing, and posting financial transactions. Accountants keep track of AP, AR, payroll, and any other financial transactions, usually in the organization’s ERP software.

Cutoff defines the boundary between time periods for accounting purposes. While it sounds simple to categorize transactions by posting date, accountants sometimes have to address timing mismatches or make other adjustments. Making sure every transaction is recorded in the correct period is essential for accuracy in closing.

Modern practice: Many organizations now automate cutoffs and enforce them through ERP integrations. Human judgment is only necessary for exceptions or ambiguous cases.

Account Reconciliations

Reconciliation is how accountants verify that the balances in the general ledger (which is the central repository within the ERP) are supported by source documents. The goal is to verify accuracy and completeness of accounting in order to address any discrepancies.

Modern practice: Reconciliation software and AI-driven transaction matching reduce manual work and surface exceptions faster. This gives the team more time to investigate and analyze discrepancies.

Accruals and Adjustments

Accruals record transactions that are understood to belong to a certain period, but haven’t been paid yet. If a contractor completes work in October, for instance, but doesn’t invoice until November, an accrual ensures that the expense appears in October’s books and not November’s.

Adjustments correct or refine previously recorded amounts. If office supplies were recorded as equipment instead of as an expense, for example, an adjustment would take care of the misclassification. Likewise, if an expense was mistakenly entered twice, an adjustment removes the duplicate.

Modern practice: Automation can handle recurring accruals. Teams can also apply materiality thresholds to automatically exclude immaterial entries.

Fixed Assets and Depreciation

Fixed assets are resources that a company uses over multiple periods (like buildings, equipment, or vehicles). They’re recorded in the ERP as assets, and not expenses, because they provide long-term value across many accounting periods.

Depreciation spreads the cost of a fixed asset over the time period that it’s used. Rather than recording the full cost of the asset upfront, a portion of the cost is recognized each period to reflect wear or obsolescence.

Modern practice: Software automates depreciation schedules and roll-forwards, and reconciles construction-in-progress (CIP) accounts and disposals by recording the necessary transactions and calculating any resulting gains or losses.

Consolidation and Reporting

Consolidation aggregates financial results across entities, subsidiaries, and business units into a set of organization-wide statements. It involves eliminating intercompany transactions, addressing foreign currency translation, and enforcing a CoA (chart of accounts).

Reporting is how accounting teams transform raw, consolidated data into formal financial statements. With valid data in hand, teams can generate compliant reports tailored to stakeholder needs without including every line item or transaction.

Modern practice: Consolidation software enables real-time eliminations and dynamic reporting dashboards, allowing teams to monitor results and proactively resolve discrepancies throughout the period, not just at close.

Key Financial Close Challenges (and How Modern Teams Solve Them)

A comprehensive modernization of your financial close starts with small wins. Component by component, pain point by pain point, implement practical changes and over time, you’ll transform your financial close process entirely.

Below are some of the most common pain points encountered by accounting teams during the financial close process.

Manual Processes and Bottlenecks

When your organization processes many thousands of transactions each month, the amount of reconciliations and journal entries piles up. If all that work is manual, it means your team is spending up to dozens of hours matching credit card or bank transactions to internal records, or calculating accruals or depreciations across departments.

The close can’t proceed until these high volume manual tasks are done, which creates a bottleneck in your workflow. Modern teams are automating much of the high-volume work, with manual reviews being reserved for cases that actually require human judgment.

Judgment is where having a competent team makes a difference. Repetitive, high-volume tasks are not. With automated matching rules and exception workflows, your team’s time will be preserved for high-value tasks. Software can handle the basic reconciliation work quickly, preventing bottlenecks.

Last Minute Adjustments and Late Reporting

It’s Friday afternoon and the close is almost done. But just as you’re preparing to close out the books, a team member identifies a batch of late invoices. These were missed during accrual, so the team has to go back and make adjustments before finalizing the close. The weekend (or your company’s IPO) can wait.

Even after the books are closed, post-close entries can delay reporting and erode confidence in your accounting team. Misclassified expenses or missed invoices, while not catastrophic, suggest a lack of rigor or process optimization somewhere upstream.

The modern, automated financial close is preferable on two fronts: first, it unburdens your team from some of the manual work that can create fatigue and lead to errors. Second, it allows for a “continuous close”, meaning that some of the reconciling and validating work can be done throughout the month, which lightens the load at month-end. Earlier error detection during the month leads to a faster month-end close and better quarter-end and year-end processes, as well.

Communication Gaps and Lack of Visibility

Teams who work in isolation miss valuable opportunities, but they also miss glaring issues. Staff accountants, FP&A, controllers, and even the CFO play distinct roles during the financial close, but when these processes aren’t sufficiently integrated, efficiency is lost. Chances to streamline are forfeited, while delays and errors slow down the close.

Tools exist to provide your team with much better visibility across the close process. Everyone from the C-suite to the most junior accounting team members can access up-data using real-time dashboards, and having a single source of truth benefits project management and cross-functional communication.

Also, consider running daily stand-up meetings during the close to align team members and maximize the utility of your tools.

Tactical and Surface-Level Analysis

If your accounting team isn’t producing high-quality, insightful reports within a few business days following month-end, the obstacle is usually time. When accountants spend days manually gathering and reconciling data, they have less capacity for investigation and analysis. That doesn’t mean investigation and analysis don’t happen, but it may mean that your team’s talents are an untapped resource.

For accounting to deliver value beyond reporting the numbers, teams need time to understand the organization’s finances deeply and translate that insight into action. Automating routine tasks frees capacity for higher-value work such as variance analysis, forecasting, and business partnership.

Numeric – the #1 automation platform for the close

.png)

Best Practices for Financial Close Optimization

A modern financial close resolves many of the pain points outlined above, but its implementation requires patience and diligence. Below are a set of proven best practices to inspire your journey toward a stronger financial close process.

Continuous Close Methodology

Learn how Nate Carbrey, VP & Global Corporate Controller at Paddle thinks about moving his team closer to the idea of a continuous or zero-day close.

The frenzy of the traditional month-end close can be alleviated by implementing a continuous close. Continuous close practices supplement the period-end close by distributing activities throughout the period.

- Reconcile daily or weekly. Reconciliations are how your team verifies that balances in your general ledger match source records. There’s no reason this process has to wait until the end of the month, and matching entries continuously saves effort when it’s time to close the books.

- Record accruals continuously. Instead of waiting for month-end, set up an automated system to post recurring accruals. For new transactions, record accruals as soon as the underlying expense or revenue is known.

- Maintain “audit readiness.” Continuous accounting helps your books remain close to audit-ready at any point. Clear documentation and automatically logged user actions maintain process and data integrity throughout the month.

This rolling approach leads to faster cycle times and more accurate interim reporting without sacrificing control or quality. At the end of the period, your team’s bandwidth can go toward better reporting and strategic advisory work.

Standardization and Process Improvement

Ad hoc processes don’t scale. When it’s time to close the books on a given period, having standardized and consistent processes pays dividends. Dedicating time to a comprehensive evaluation now can save your team hours at each close going forward.

- Unify close policies. Apply consistent rules for reconciliations, cutoffs, and approvals across all entities and regions. Enforce these rules automatically wherever possible.

- Review recurring entries. Recurring entries like monthly rent or depreciation should periodically undergo a zero-based review to ensure accuracy and eliminate obsolete or immaterial entries.

- Document and train. Maintain clear standard operating procedures and training materials. Keep these resources centralized and accessible to reinforce accountability.

Standardization improves accuracy and reduces the need for follow-ups or ad hoc communication. It also supports scalability as your organization and accounting team grow, or you add new business units.

Technology and Data Management

Effective accounting depends on the availability of good data. Technology enables this, but it doesn’t guarantee positive outcomes without the right processes in place.

- Create a single source of truth. Connect your ERP, CRM, BI, expense management, and analytics tools through integrations. Integrating these systems helps preserve your ERP as the single source of truth.

- Automate validations and controls. Detect data errors or duplicated transactions upstream, in real time, before they reach the general ledger.

- Use specialized platforms. Close-management and smart-subledger platforms simplify complex processes like revenue recognition and intercompany eliminations. Identify the areas where your close typically encounters bottlenecks, and explore purpose-built solutions.

Structuring your data environment to reduce downstream corrections will alleviate your accounting team’s biggest headaches. Additionally, fewer errors will promote confidence in your analysis and reports.

Team Development and Change Management

The purpose of improving your financial close process is to deliver better outcomes. The actual delivering is done by your team; it’s important to make sure they’re motivated to execute on all significant procedural changes.

- Create transparency around changes. Explain the “why” behind new systems and workflows. Help your team connect the dots between the change, the new desired state, and how it will help the team’s performance.

- Cross-train team members. Provide your team with training to handle multiple close activities and oversee multiple automated systems. During the close period, responsibilities and bandwidth can be flexed to improve speed.

- Invest in your people. Encourage professional development in analytics, business partnering, and advisory skills. Having context for these activities will allow team members to be proactive when opportunities arise to shift away from repetitive tasks.

Motivated, flexible teams are better suited to the continuous change that is required to optimize the financial close and other accounting tasks. As technological changes yield results, your team should be ready to build on this success and optimize even further.

Leveraging a Close Calendar and Process Framework

A structured close calendar turns best practices into consistent habits. It ensures accountability, transparency, and accuracy in forecasting timelines.

Designing Your Close Timeline

A formalized, rolling close calendar defines each activity, owner, and deadline in the overarching close process. It includes lists of pre-close activities, close-day tasks, and post-close steps.

Days -5 to 0: Pre-close activities including data validation, accrual preparation, and subledger reconciliations.

Days 0 to 2: Close-day tasks like journal postings, intercompany eliminations, and final review.

Days 2 to 4: Post-close steps such as variance reporting and audit documentation.

Modern teams often map these activities to a shared dashboard or project management platform that updates in real time with a RACI matrix attached, which ensures all stakeholders can track progress.

Assigning Roles and Responsibilities

A RACI (Responsible, Accountable, Consulted, Informed) matrix clarifies ownership of tasks and prevents duplicate efforts or missed handoffs. It also enforces accountability for timelines.

Key roles include:

- Close manager: Oversees the timeline, approvals, and status reporting.

- Reconciliation owners: Complete and certify assigned accounts.

- Reviewers and approvers: Verify accuracy and completeness before sign-off.

Note that RACI applies at the task level, not at the level of the close process itself. Clearly defining responsibilities for every task, however, contributes to a well-managed close.

Creating Effective Close Checklists

Checklists serve two purposes: expressing the totality of a project’s scope and tracking progress toward completing that scope. Meet both with a checklist that includes all required tasks with dependencies, due dates, and completion status directly attached, as well as escalation procedures for delayed or blocked tasks.

When combined with a standardized process, strong governance, and awareness of the capabilities of your tools, the close calendar and checklist become the backbone of a predictable, high-performance close.

Leveraging Automation and AI in the Financial Close Process

Automation and AI work hand-in-glove to deliver a superior financial close. By leveraging finance automation and AI, your close will be faster, easier, and more impactful for the stakeholders who depend on your accounting team’s outputs.

Identifying Automation Opportunities

In the past, it was safe to assume that speed and accuracy were necessary inverse trade-offs. Automation challenges that assumption; it’s now possible to find processes that are both faster and more accurate.

AI and machine learning tools now process transactions, reconcile accounts, and generate basic reports in a fraction of the time. When compared with humans, software is simply better at certain tasks (primarily, repeatable ones). Humans, on the other hand, are better at complex tasks requiring judgment and context.

Which of the tasks in your financial close process are suitable for AI assistance? Look for:

- High volume and frequency

- High rule clarity (i.e., how well the tasks follows logic/rules)

- Clean, structured data

- Low error impact (i.e., errors aren’t necessarily catastrophic)

- Ease of tracking, review, and approval

- Low judgment or interpretation requirement

Bank account reconciliations, recurring journal entries posting, intercompany eliminations, and variance calculation are just a few tasks that might meet the criteria listed above.

AI-Powered Close Capabilities

AI has several valid use cases when it comes to executing the financial close. Embedding AI into your workflows makes the slowest processes faster while also flagging errors earlier.

AI models can analyze historical data patterns to detect irregularities before they appear in reconciliations or reports. These systems can study each account, department, or time period, then flag anomalies (like duplicate journal entries, missing accruals, or unusual expense spikes) automatically.

Variance and flux analysis can also be enhanced by AI. It can surface material flux or variance and generate basic analysis for your team to base further investigation on.

Issuing reports based on findings is one of the core activities of an accountant, but that doesn’t mean you need to reinvent the wheel each time a financial close comes around. AI can draft simple reports supported by the data, which your accounting team can then use to communicate key insights to stakeholders or draft more detailed commentary.

Implementation Approach for Close Automation

Implementing AI, automation, and integration platforms drives value, but it isn’t necessarily easy. To attain organization buy-in, begin by persuading members of your team and organization of the value of these tools with small wins. Automate bank reconciliations and recurring entries, then present the ROI and suggest further opportunities for similar improvements.

Every pilot program or trial implementation should have measurable (and attainable) KPIs attached. As these tools prove their value, be ready with a strategic scaling roadmap, taking care to factor in team readiness as more and more of the burdensome tasks within the financial close are automated.

Selecting Close Management Software

Best-in-class close management software can lead to profound benefits for the close process and, in turn, for your organization. But before you choose a vendor, be sure to find the right tool for your needs.

Key evaluation criteria include ERP integration (and depth of that integration), automation capabilities, ease of use, time to value, implementation and support quality, and licensing model.

It’s also possible to build your own platform or use a hybrid build/buy approach, though there are pitfalls when bringing development in-house. A purpose-built, AI-powered solution like Numeric includes support and implementation assistance, as well as deep ERP integrations with common platforms like NetSuite.

How Numeric Helps Modernize the Financial Close Process

Numeric is an AI-powered close automation tool for complex accounting teams that want to modernize their financial close.

We’ve built our platform to address the most urgent pain points in the financial close process:

- Automate reconciliations & recurring entries to eliminate manual bottlenecks

- Ensure audit readiness with built-in controls, documentation, and audit trails

- Improve collaboration & visibility through close calendars, dashboards, and task ownership

- Accelerate reporting so finance teams deliver insights in days, not weeks

- Enable your team to focus on strategy and impact instead of low-effort, time-consuming tasks

See how Numeric helped Hadrian achieve a 67% improvement in close timeline efficiency.

Conclusion

The financial close drives business decisions, and without it, your organization would be financially adrift. The close turns data into insights, which inform reporting and eventually drive decision-making at the C-suite level.

So, the best teams deliver insights quickly and error-free. In order to do that, they limit bottlenecks by putting AI and automation software in charge of the tasks that don’t benefit from human judgment. There are actually many of these tasks, but there are also tasks where judgment, context, and human interpretation do make a difference. The best teams invest in these too.

In addition to automating routine, fatigue-inducing tasks, technology enables new capabilities like continuous reconciliation and real-time visibility through shared dashboards. Your accounting team can reach the close faster with these tools, while also delivering greater value across the wider organization throughout the period.

With Numeric, accounting teams can master the financial close, stay audit ready, and provide substantial value through strategic analysis. A happier, more effective, and more cross-functionally engaged accounting team is possible with Numeric.

Related Content

The Finance Engineer: Why Accountants Are the Best Builders in the Room

Why accountants, not engineers, are becoming the best builders on modern finance teams. Meet the Finance Engineer.

.png)

Numeric vs. Ledge: What's the Best Close Platform for Your Business?

A detailed comparison of Numeric and Ledge, two modern close management platforms, covering features, architecture, pricing, and a framework for choosing the right fit for your team.

.png)

What is Record to Report: Process, Steps, and Benefits

Learn how the Record to Report process works, from transaction capture to financial reporting. Discover steps, challenges, automation strategies, and best practices for modern accounting teams.