Cash Runway In 2026: Formula, Analysis, And How To Extend It

.png)

Every CFO and Controller has been in some version of the same dreaded meeting. The board wants to know how much time the company has. And not in the abstract, but in months, with assumptions they can stress-test and a number they can trust.

Cash runway is the metric that answers that question. But the answer is only as reliable as the data behind it, and for many finance teams, that's where things break down. Reconciliations lag, and cash data sits fragmented across bank accounts, entities, and ERPs. This means your close takes two weeks, and the runway number leadership sees is already stale by the time it reaches a slide deck.

This guide covers everything you need to know about cash runway, including what it actually measures, how to calculate it correctly, and how to analyze it (and leverage it!) correctly.

Key Takeaways

- Cash runway measures how long a company can operate at its current burn rate before running out of cash.

- Calculating runway is straightforward (divide available cash by monthly net burn), but the judgment calls around what counts as "available" and how to normalize burn are what determine whether the number is actually useful.

- Runway built on unreconciled cash balances or an incomplete close is a guess dressed up as a metric. The quality of your reconciliation process is the foundation of trustworthy runway reporting.

- A single-point runway snapshot isn't enough for real decision-making; finance leaders should pair runway with scenario modeling, rolling 13-week cash forecasts, and a defined recalculation cadence tied to the close.

- Extending runway starts with working capital improvements and surgical spend review, not across-the-board cuts that weaken the functions keeping the business running.

What Is Cash Runway?

Every CFO and Controller has been in some version of the same dreaded meeting. The board wants to know how much time the company has. And not in the abstract, but in months, with assumptions they can stress-test and a number they can trust.

Cash runway is the metric that answers that question. But the answer is only as reliable as the data behind it, and for many finance teams, that's where things break down. Reconciliations lag, and cash data sits fragmented across bank accounts, entities, and ERPs. This means your close takes two weeks, and the runway number leadership sees is already stale by the time it reaches a slide deck.

This guide covers everything you need to know about cash runway, including what it actually measures, how to calculate it correctly, and how to analyze it (and leverage it!) correctly.

Cash runway measures how long a business can continue operating before it runs out of cash, based on its current or projected burn rate. Take the cash you have, divide by how fast you're spending it, and you get a time horizon.

What makes runway strategically important is what it represents. For a CFO, runway is a measure of optionality: how much time leadership has to hit milestones, adjust plans, negotiate financing, or raise capital before the math stops working. A company can look healthy on the P&L and still face a runway problem if collections lag, obligations bunch up, or revenue recognition doesn't align with when cash actually arrives.

Why Runway Matters Beyond Startups

Runway often gets framed as a startup metric, since startups are typically strapped for cash and are in aggressive growth mode. And this makes sense, since 70% of startups fail because they run out of capital.

But that framing sells it short, because any organization with cash flow variability benefits from tracking it. That includes SaaS companies managing annual billing cycles, but it also includes multi-entity businesses with fragmented cash pools and project-based firms with lumpy revenue.

In practice, runway informs headcount planning, capex decisions, vendor payment timing, and lender conversations. It belongs in the strategic finance toolkit alongside cash flow forecasting and working capital analysis.

Cash Runway vs. Related Metrics

Runway is just one important metric that brands need to account for. It's also adjacent to a few other financial numbers your team may be tracking, so here's a breakdown of other essential metrics and how they relate to cash runway:

The table above highlights an important relationship. Burn rate feeds into runway, but neither tells you much about week-to-week liquidity. That's where a 13-week cash forecast comes in, testing whether the headline runway number actually holds up against real-world inflow and outflow timing.

How To Calculate Cash Runway Correctly

The formula itself takes about ten seconds to explain. The judgment calls that make it accurate take considerably longer.

The Standard Formula

This is the standard formula for calculating cash runway:

Cash Runway (in months) = Available Cash ÷ Monthly Net Burn Rate

And to make sure you're running the right calculations, two definitions matter here:

- "Available cash" should include only unrestricted cash and equivalents that are realistically deployable for operations. Restricted balances, debt reserves, escrow accounts, and cash trapped in foreign entities with repatriation constraints should be excluded.

- "Net burn" is total monthly cash outflows minus total monthly cash inflows. This is the most common input for runway reporting. Gross burn (total outflows only, ignoring inflows) is useful as a downside lens because it shows your fixed cash commitments if revenue disappeared tomorrow.

One common mistake to avoid is overstating runway by mixing accrual-based revenue assumptions or non-cash offsets into what should be a purely cash-based burn figure. If stock-based compensation, depreciation, or accrual-only entries are influencing your burn number, the runway output won't reflect reality.

What This Looks Like: An Example Of A Cash Runway Calculation

Say your company has $12M in unrestricted cash, $900K in monthly operating outflows, and $400K in monthly cash inflows.

- Net burn: $900K − $400K = $500K/month

- Runway: $12M ÷ $500K = 24 months

That looks comfortable and seems to give you some solid breathing room.

But then you adjust it for context, and realize you need to account for a $200K annual insurance payment that hits next month, you're planning three hires at $15K/month each in loaded cost, and a large customer payment ($150K) is 60 days overdue.

Suddenly, the next six months of effective burn look closer to $600K–$650K, and runway drops to 18–20 months. The formula didn't change, but the input did get more honest.

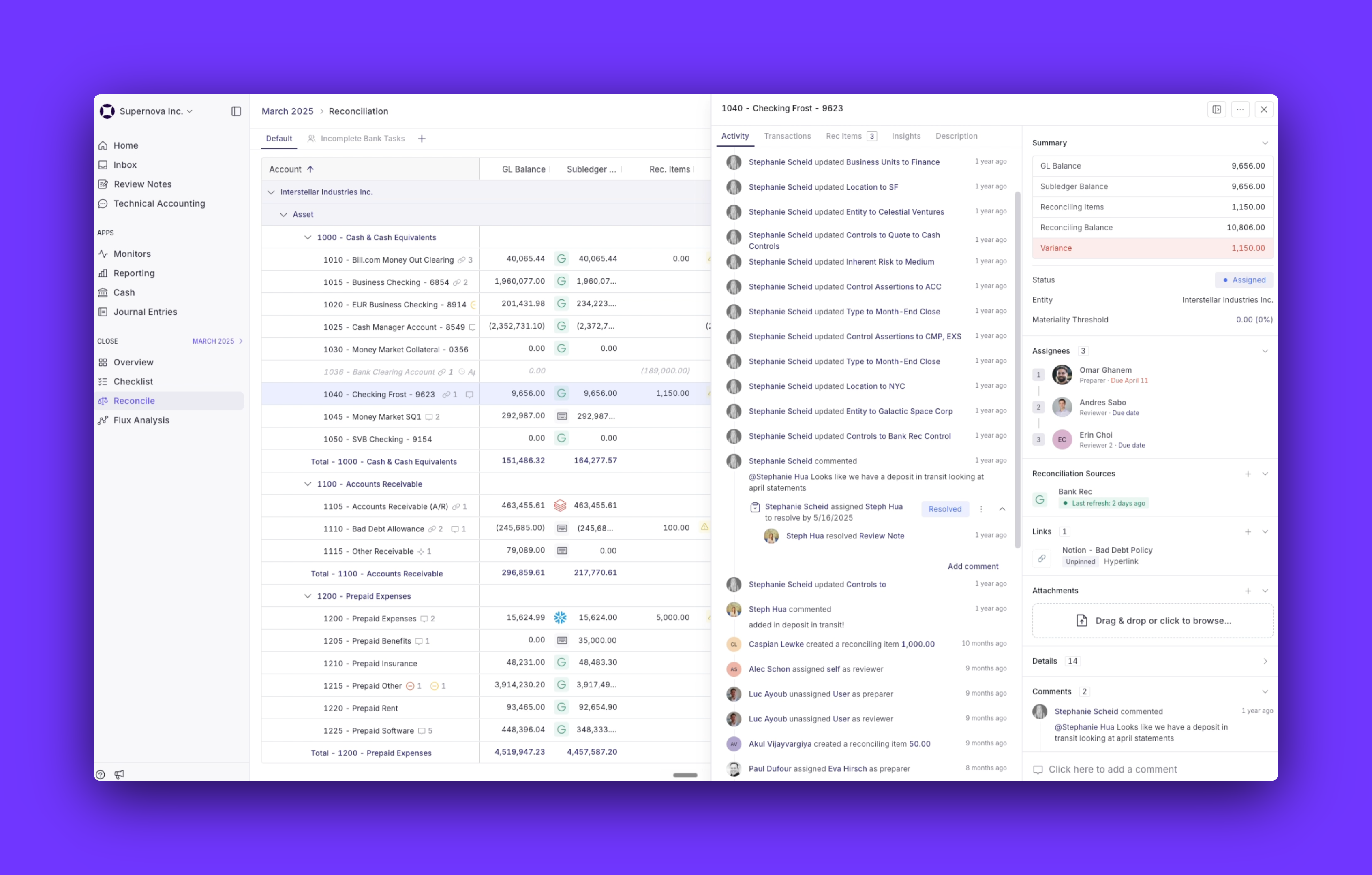

Why Accurate Reconciliations Are Foundational To Reliable Runway

If the starting cash balance is unreconciled or the close is incomplete, the runway number is essentially a guess with a formula wrapped around it.

How Bad Inputs Compound in Cash Runway

For teams still building burn rate calculations in Excel, errors tend to compound quietly — a miscategorization in one month shifts the average, and that average feeds every projection downstream. Unreconciled transactions, duplicate entries, stale bank balances, and misclassified cash movements can all distort the "available cash" numerator.

And the same principle applies to the denominator. If expenses are miscategorized or timing mismatches remain unresolved, the monthly burn average becomes unreliable — and your most senior people end up spending close time validating figures instead of doing the analysis that actually moves the needle. A small error in either input can materially shift your runway when it's projected over 12 or 18 months.

This is the chain that produces actually trustworthy runway projections:

- Bank feeds and statements move to bank reconciliations

- Reconciliations create validated cash balances

- Validated cash balances mean a clean close

- A clean close means reliable cash flow analysis

- That accurate cash flow analysis gives you defensible runway metrics

Pre-Calculation Data Hygiene Checklist

Before running a runway calculation, it's time for a quick data hygiene checklist. Finance teams shouldn't start crunching any numbers until they confirm that:

- All key bank accounts are reconciled through the reporting date

- Large reconciling items and aged outstanding items have been validated

- One-time inflows and outflows have been identified and either normalized or explicitly modeled

- Restricted cash, debt reserves, and intercompany cash are treated correctly and have been excluded from available cash

- Recent journal entries that affect cash accounts have been reviewed and posted

Faster Close = Fresher Runway

There's a direct relationship between close speed and runway accuracy. If the close takes 15 business days and runway recalculation waits on the close, leadership is making decisions based on data that's already half a month old.

This is where continuous accounting practices make a meaningful difference. Teams that move reconciliations and monitoring forward in the month produce cash data that's more current and trustworthy. Accelerating the financial close process is itself a runway lever, shrinking the lag between reality and the number being reported — and giving Controllers a runway figure they can stand behind when leadership asks, not one they have to caveat before presenting it.

Numeric: the #1 tool for continuous closes

.png)

How To Analyze Cash Runway

A single-point runway number tells you something useful, and that's a good start. Understanding how quickly that number can change and why is where the real analytical work begins. Let's look at what you can actually learn from your cash runway when you analyze it correctly.

Trend It Over Time

Track runway month-over-month or quarter-over-quarter. It can help you understand what's happening with your business's finances.

A company that's reported "18 months of runway" for three consecutive quarters is in a very different position than one where runway has dropped from 18 to 14 to 10.

Pair the runway trend with burn-rate trend lines and major drivers of change to give leadership a complete picture of what's happening and what's changing.

Build Scenarios Instead of Single Estimates

Pressure-test your runway by changing assumptions.

What happens if collections slow by 15%? Or what if you accelerate two planned hires?

A simple scenario table makes the sensitivity concrete. Here's what that might look like:

Pair Runway With a Rolling 13-Week Cash Forecast

Runway gives your team the long view, but a 13-week forecast gives operational precision on near-term inflows and outflows.

The two work together. Runway frames strategic options while the short-term cash forecast surfaces immediate liquidity pinch points. Boards and lenders increasingly expect this level of short-term cash visibility, particularly as higher financing costs and longer fundraising cycles have made liquidity risk harder to manage with quarterly snapshots alone.

Recalculate on a Defined Cadence

At minimum, recalculate runway monthly and tie it to the close.

Specific events should also trigger off-cycle updates, including:

- Financing events

- Missed large collections

- New hires or layoffs

- Covenant changes

- Significant capex

- Customer concentration shocks

Restricted Cash, Credit Facilities, and Venture Debt

Not all cash on your balance sheet is available to fund operations, and not all liquidity sources belong in the same category. When calculating runway, it helps to think in three buckets:

- Unrestricted operating cash: Cash you can deploy for day-to-day operations without conditions or approval. This is your runway numerator.

- Restricted balances: Debt reserves, escrow accounts, collateral deposits, and cash held in foreign entities with repatriation constraints. These sit on the balance sheet but aren't available to cover next month's payroll.

- Undrawn liquidity sources: Lines of credit, venture debt facilities, or receivables financing arrangements. These can extend runway on paper, but only if covenants are met, draw conditions are realistic, and repayment timing doesn't create a new cash crunch downstream.

Watch AR, AP, and Lumpy Cash Patterns

Slow collections can erode effective runway faster than a clean P&L might suggest. Conversely, delayed AP payments can temporarily flatter the runway outlook, even though those obligations are still coming.

Annual prepayments, payroll cycles, bonus timing, tax remittances, and deferred revenue also create "lumpy" cash patterns that distort simple monthly averages. Deferred revenue improves cash today, but it doesn't make future delivery obligations disappear. Normalize these items or model them explicitly rather than burying them in an average burn figure.

For multi-entity businesses, a group-level runway number can mask a cash trap at the entity level. If $8M of your $12M in cash sits in an entity with repatriation constraints, for example, your effective runway is very different from what the consolidated number suggests. This is why intercompany reconciliation is so crucial for large multi-entity organizations.

What Is a Healthy Cash Runway?

So, what exactly is a healthy cash runway?

The honest answer depends on your business model, stage, financing access, and how predictable your cash flows are.

Benchmarks Aren't a One-Size-Fits-All

The commonly cited guideline for venture-backed companies is 12–18 months of runway. But a pre-revenue startup burning through seed funding has a very different risk profile than a profitable SaaS company with $50M ARR and a credit facility.

Gross margin, collections predictability, and the current fundraising environment all influence what "healthy" actually means.

A Threshold-Based Action Framework Based On Your Cash Runway

Rather than anchoring to a single benchmark, consider a framework tied to approximate milestones:

One important nuance here is that "operational runway" often ends well before the cash balance hits zero. Board expectations, lender covenants, and vendor confidence all create pressure to act with significant cash still in the bank.

One Number + Many Audiences = Multiple Interpretations

How you present runway should change depending on who's in the room.

A board wants to see the base-case number alongside downside scenarios, with clear triggers for when management would shift strategy. They're evaluating risk, so show them the assumptions that would change the picture and what actions you'd take at each threshold.

Investors care about milestone timing. They want to know whether the company has enough runway to hit the next inflection point, whether that's a revenue target, a product launch, or a fundraising milestone. Lead with the relationship between runway and the milestones that drive valuation.

Internal operating leaders need budget guardrails. They're less interested in the overall number and more interested in what it means for their hiring plans, project budgets, and spending authority. Give them the "so what" directly: "At current burn, we have flexibility to backfill two roles this quarter, but a third would need to wait until Q3 collections land."

In every case, presenting runway as a single number without the underlying assumptions invites misinterpretation. Include the collections assumptions, hiring plans, and key sensitivities alongside the headline figure.

How To Extend Cash Runway

The best runway strategies preserve liquidity while protecting the activities that drive the most value.

Start with working capital. Faster collections, tighter billing discipline, improved invoice accuracy, and negotiated vendor terms often extend runway faster and with less organizational damage than broad cost cuts. Think annual prepay discounts, milestone billing, or escalation processes for aging AR.

Cut surgically, not across the board. Segment spend into mission-critical, efficiency-positive, and deferrable categories. Software sprawl, low-ROI marketing, and open headcount in non-core functions are common starting points. Flat percentage cuts that weaken close quality or revenue operations tend to create bigger problems than they solve.

Pull cash forward through revenue and pricing moves. Upfront billing, revised payment terms, or packaging changes can improve near-term cash without necessarily increasing volume. A billing structure change can affect runway sooner than a broader go-to-market initiative.

Consider non-dilutive financing. Venture debt, receivables financing, lines of credit, or asset sales can extend runway, but each comes with tradeoffs around covenants, repayment timing, and signal risk.

Common Cash Runway Mistakes

Most runway failures aren't formula errors. They're input, process, or interpretation problems.

- Using stale or unreconciled cash data. Presenting runway before bank recs, intercompany adjustments, or cash journal entries are complete creates inaccuracies. The right question isn't just "what is our runway?" but "how confident are we in that number?"

- Treating burn rate as static. A flat historical average can mislead when hiring, seasonality, or one-time projects are about to change the cost structure. Rolling averages and forward-looking assumptions create a better model.

- Ignoring non-cash items. Depreciation, amortization, and stock-based compensation matter for profitability analysis but must be stripped out of cash-based runway calculations.

- Conflating balance sheet cash with deployable cash. Restricted balances, debt reserves, escrow accounts, and cash in entities with repatriation constraints all inflate the "available cash" number if they're not excluded.

- Reporting a number without the assumptions. A runway figure presented without collections assumptions, hiring plans, or downside scenarios is a number without context. Include "runway confidence" or assumption sensitivity alongside the headline figure.

How Numeric Helps Teams Build More Trustworthy Runway Reporting

Numeric supports the inputs that make runway reliable. The platform unifies close management, account reconciliation, cash matching, and cash visibility into a single workflow, so the data feeding your runway calculation is reconciled, current, and auditable. With Numeric's MCP, finance teams can also trigger close workflows and surface cash data directly from their AI client — so runway inputs stay current without manual context-switching between tools.

When reconciliations happen faster and exceptions are resolved earlier, the gap between "what happened with our cash" and "what does that mean for our runway" shrinks significantly. And with CFOs struggling with a financial talent shortage, this kind of software can help speed up manual processes and reduce errors so their team can focus on the strategic decision-making.

Better reconciliation discipline leads to better cash flow management, which leads to runway numbers that hold up in board meetings, investor conversations, and internal planning sessions.

Turn Cash Runway From a Formula Into a Finance Control

Cash runway is one of the most important numbers a finance leader communicates. But the real value isn't in the formula itself. It's in the ability to produce that number quickly, defend it confidently, and update it when conditions change.

That requires reconciled cash data, normalized burn assumptions, scenario discipline, and a close process fast enough that the number is still relevant when it reaches a decision-maker. Better reconciliations lead to better forecasts, which lead to better runway decisions.

If your current process leaves you questioning the number before you present it, that's worth fixing. See how Numeric can help.

Frequently Asked Questions

Related Content

.png)

How to Build an AI Audit Trail for Your Accounting Workflows

A practical guide to AI audit trails for accounting: what to capture, why SOX, PCAOB, and GAAS require traceability, and how to audit AI agents and skills, not just AI features bolted onto your close software.

.png)

Finance Data Warehouse: What It Is and Why It Matters

What a finance data warehouse is, where it fits alongside your ERP, and how it helps the month-end close.

.png)

NetSuite Custom Reports: How to Build Your Own

A step-by-step guide to building custom reports in NetSuite — Report Builder, Financial Report Builder, saved searches, SuiteAnalytics Workbook, and where native reporting hits its limits.