Revenue Recognition Automation: From ASC 606 Compliance to a Faster Close

.png)

Revenue recognition is one of those workflows that looks manageable until it isn't. At 20 contracts, a capable accountant can decode performance obligations, allocate prices, and post entries manually.

At 200 — with amendments, renewals, and variable consideration layered on top — the same process becomes a liability. One missed modification corrupts your deferred revenue balance. The error propagates. You find it at audit.

Hiring more accountants doesn't change the math. Manual recognition degrades as contract volume grows. The spreadsheet that worked at Series B doesn't survive the complexity of Series D. For SaaS companies with multi-element arrangements, revenue recognition alone can consume two to three days of a typical close — time your team can't buy back by working harder.

Revenue recognition automation is the infrastructure that replaces it. Here's how it works, what it costs to skip, and how to implement it effectively.

New to the standard itself? Our guide to revenue recognition for SaaS covers the ASC 606 fundamentals, including the five-step model, deferred revenue mechanics, and contract modifications, before you automate them.

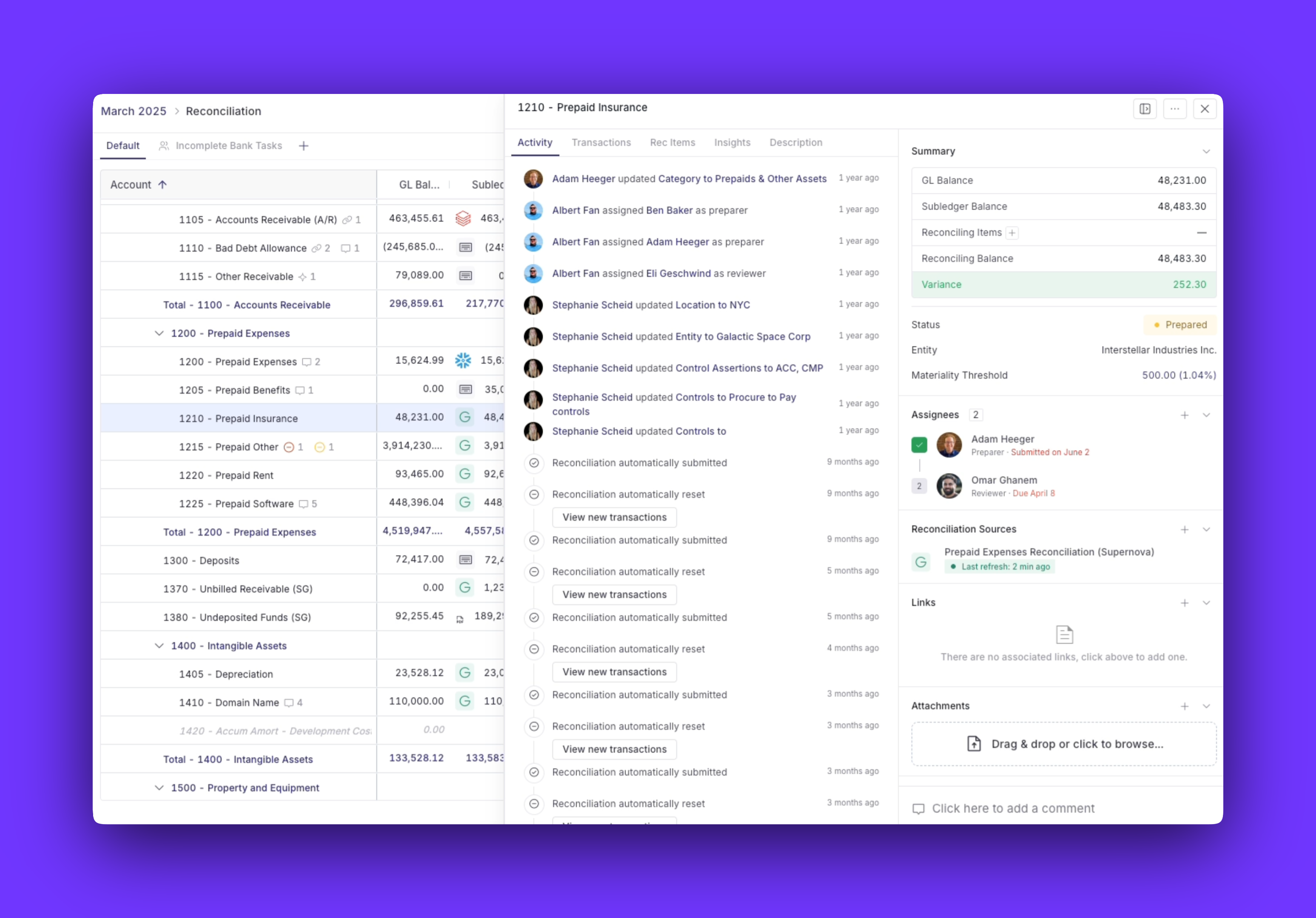

What Is Revenue Recognition Automation?

Revenue recognition automation is a dedicated financial infrastructure layer that removes the manual work from your close. Instead of your team decoding obligations and posting entries contract by contract, the software does it — consistently, every period, across every contract in your portfolio.

It runs on ASC 606 and IFRS 15, the standards that govern when and how revenue gets recognized. Every allocation, every journal entry, every deferred balance follows the same rule set.

How It Differs From Manual Revenue Recognition

Manual revenue recognition requires human interpretation, contract by contract. An accountant reads each arrangement, identifies performance obligations, determines standalone selling prices, allocates the transaction price, and posts journal entries sequentially — applying judgment case by case.

Automation applies a single configured rule set simultaneously across the entire contract population. The system doesn't read contracts differently each month depending on who's working. It applies the same logic to the 500th contract that it applied to the first.

That repeatability is the compliance architecture, not just a speed advantage.

The Five-Step ASC 606 Model, Automated

ASC 606 prescribes a five-step framework for every revenue transaction. Here's what automation executes at each step:

- Contract identification. The system ingests contract data from your CRM or billing platform and validates whether the arrangement meets ASC 606 criteria — commercial substance, collectability, and approved terms.

- Performance obligation identification. The system applies your configured rules to determine whether promises are distinct — separating, for example, a software license from an implementation service from a support subscription.

- Transaction price determination. The system calculates total contract consideration, adjusting for variable components such as usage-based pricing, contingent fees, and discounts, using your SSP methodology.

- Transaction price allocation. The system allocates the total price across obligations in proportion to their relative standalone selling prices — no manual SSP matrix required.

- Revenue recognition. The system monitors delivery milestones or time-based fulfillment and posts journal entries to the GL for each obligation as it is satisfied.

The sequence looks clean on paper. The complexity is in the exceptions — amendments, variable consideration, bundled obligations that may or may not be distinct. Automation holds the logic consistent when the contracts stop being straightforward.

.png)

Revenue Recognition Automation Benefits for Finance Teams

Here's how automation changes the equation across the dimensions that matter most to your close:

| Criteria | Automated Recognition | Manual Recognition |

|---|---|---|

Accuracy |

Consistent rule application across all contracts | Dependent on individual judgment per contract |

Compliance documentation |

Timestamped at the moment of each recognition event | Reconstructed at audit time |

Close speed |

Constrained only by data feed latency | Limited by human processing capacity |

Scalability |

Maintains consistency regardless of volume | Degrades as contract volume grows |

Compliance With ASC 606 and IFRS 15

The compliance mechanism that matters most isn't the one that handles standard arrangements correctly. It's the one that handles non-standard arrangements correctly.

A well-configured recognition engine flags contracts that don't fit the standard rule set for human review, instead of applying a default that may be wrong. That distinction is where most bolt-on recognition modules fail. They apply a default, log no exception, and move on — which means the misclassification sits in your deferred balance until someone finds it.

An engine that can't tell the difference between "I processed this correctly" and "I applied a default because I didn't know what else to do" isn't a compliance control. You just can't see the damage until audit week. And by then, the path to correction runs through an audit adjustment or a restatement — not a journal entry.

If you're planning an IPO, your recognition workflow will be under a microscope before you ring the bell. See what auditors actually look for.

Scalability and Revenue Forecasting

Automated systems process contract modifications in real time and maintain a deferred revenue waterfall that reflects the current state of every contract. That waterfall informs CFO-level decisions — revenue forecasts, ARR movements, cohort analysis — without requiring a manual refresh cycle before each planning session. For Controllers at SaaS companies, this is the difference between FP&A getting ARR figures on demand versus opening a Slack thread asking when the numbers will be ready.

Revenue Recognition Best Practices

Automation amplifies existing policies. Undocumented or inconsistently applied recognition rules become a configuration liability at scale. A judgment call that one accountant makes is correctable on a case-by-case basis. A judgment call baked into the system configuration propagates to every contract processed thereafter.

Before Implementing Revenue Recognition Automation

- Document SSP methodology for every product and service offering

- Map all active contract types to performance obligations

- Establish a policy for contract modifications (prospective vs. cumulative catch-up)

- Validate integration between your CRM, billing platform, and the recognition engine

- Test recognition output against manually computed results for a representative contract sample

After Implementing Revenue Recognition Automation

- Run parallel processing for at least one full period before decommissioning manual schedules

- Establish exception routing protocols for contracts that the system escalates

- Confirm audit trail completeness on a sample of recognition events

- Review the deferred revenue roll-forward monthly and reconcile to the GL

Reconciling Recognized Revenue to the GL After Close

Revenue recognition automation handles the allocation and posting. What it doesn't handle is verifying that the entries that landed in the general ledger are correct — and that deferred and recognized revenue balances tie before the books close.

That is a distinct workflow from recognition itself, and it belongs to the close team.

Numeric's reconciliation product pulls live trial balance and subledger data directly from your ERP, supporting transaction-level drill-down on tie-out breaks and surfacing the exact transaction behind a discrepancy — without a manual GL export search.

For Soundstripe's accounting team, that search used to mean manually reconciling 100+ balance sheet accounts each month. After moving to a single platform with live ERP data, the team streamlined reconciliations and went into audit with controls and reliable numbers they could actually stand behind.

The recognition engine posts the entry. The reconciliation layer confirms that it is correct.

Beyond reconciliation, teams that want to catch recognition issues mid-period — before they compound — use Numeric's Transaction Monitors to flag transactions hitting deferred revenue accounts that fall outside expected patterns. An amendment that posts mid-period and doesn't follow your standard recognition logic gets surfaced immediately, not at close.

What to Look for in Revenue Recognition Automation Software

There's a real difference between a billing platform with a recognition module bolted on and a system built specifically for this work. The former handles the easy cases. The latter holds up when the contract gets complicated — and under audit scrutiny.

| Capability | What to Look For |

|---|---|

Obligation identification |

Configurable rules for distinct vs. non-distinct determinations, not just template-based bundling |

SSP methodology support |

Multiple methods (VSOE, adjusted market assessment, residual approach) with audit-defensible documentation |

Contract modification handling |

Prospective and cumulative catch-up options, not a single default |

Exception flagging |

Automated escalation for non-standard arrangements with full audit trail |

Deferred revenue roll-forward |

Real-time waterfall view, not a periodic batch export |

Audit trail |

Timestamped event log for every recognition decision, accessible by auditors without data preparation |

Integration With ERP, CRM, and Billing Platforms

A recognition engine allocates and posts correctly. But those entries flow into the same GL your broader close team is reconciling. If the sync between the recognition layer and ERP is manual or delayed, data integrity breaks down at exactly the handoff where it matters most.

Before evaluating any platform, name the relevant systems you need connected: CRM (Salesforce is the standard for most SaaS companies), billing (Stripe, Zuora, and Chargebee cover most subscription architectures), and ERP (NetSuite is the standard for most mid-market SaaS companies; Sage Intacct is common in nonprofit and healthcare).

A recognition engine that can't pull contract data from your billing system without a manual export will create the same reconstruction problem you were trying to solve.

On the close management side, Numeric integrates with NetSuite, Xero, QuickBooks Online, and Sage Intacct — pulling every transaction line in real time. That means the reconciliation layer, which verifies recognized and deferred revenue balances against the GL, is working from live data, not a batch upload. That matters when an amendment posts mid-period and the GL reflects it before the reconciliation cycle runs.

On the analysis side, once recognized and deferred revenue balances are confirmed, Numeric's Flux Analysis product surfaces the exact transactions driving period-over-period changes — so the question "why did recognized revenue move this month?" has an answer before the CFO asks it.

The Future of Revenue Recognition Automation in Financial Operations

Finance teams adopting recognition automation now are building the data foundation that enables real-time board reporting and predictive revenue analytics.

The AI capabilities emerging in this space are worth watching with appropriate specificity. Anomaly surfacing — flagging recognition patterns that deviate from historical norms — is already present in leading platforms. Mid-period misclassification flagging, where the system identifies contracts that may have been allocated incorrectly based on subsequent data, is an active development area.

Teams already connecting their AI clients to Numeric via MCP are running these workflows today — cross-referencing recognized revenue against contract data in Drive, triggering anomaly scans mid-period, and routing exceptions to the right reviewer in Slack, all without leaving their AI tool of choice. The Numeric MCP ships with pre-built skills for revenue workflows including accrual drafting, JE generation, and variance investigation — and customers are building their own on top.

The durability argument for FASB interpretive updates is practical, particularly for pre-IPO companies. Systems that receive rule updates centrally maintain compliance without requiring manual policy rewrites after each regulatory change. When the FASB issues new guidance on variable consideration or contract modification accounting, a centrally updated platform automatically reflects the change across your entire contract population.

The future capabilities are worth tracking. But the more pressing question is what breaks in your current recognition workflow when contract volume doubles — and who finds it first, you or your auditors.

From Recognition to Close: Where Automation Ends and Your Team Picks Up

A dedicated revenue recognition engine owns the ASC 606 workflow: obligation identification, price allocation, fulfillment monitoring, journal entry posting, and the timestamped audit trail that documents every decision.

That is the recognition layer.

What happens after those entries post — verifying balances, reconciling the GL, closing the books — belongs to the close management layer. These are distinct workflows, and conflating them creates gaps in both.

That post-recognition layer is exactly what Numeric is built for. Once the recognition engine posts the entry, Numeric pulls live transaction data from your ERP, surfaces the exact discrepancy that caused the balance to break, and provides your team with a timestamped audit trail before the books close.

The tie-out, the exception surfacing, the audit trail — that's where the close is won or lost.

Frequently Asked Questions About Revenue Recognition Automation

Related Content

The Finance Engineer: Why Accountants Are the Best Builders in the Room

Why accountants, not engineers, are becoming the best builders on modern finance teams. Meet the Finance Engineer.

.png)

Numeric vs. Ledge: What's the Best Close Platform for Your Business?

A detailed comparison of Numeric and Ledge, two modern close management platforms, covering features, architecture, pricing, and a framework for choosing the right fit for your team.

.png)

What is Record to Report: Process, Steps, and Benefits

Learn how the Record to Report process works, from transaction capture to financial reporting. Discover steps, challenges, automation strategies, and best practices for modern accounting teams.