Revenue Recognition for SaaS: The ASC 606 Guide That Holds Up Under Audit

.png)

At some point, every SaaS accounting team hits the same wall. The business is growing, contracts are getting more complex, and what used to be a simple "did they pay? great, book it" process is now requiring a level of precision the old one wasn't built for.

Bundled SKUs, annual contracts paid upfront, mid-period upgrades, free trials that convert — every new pricing variation adds another layer to the question of when revenue is actually earned.

That question has a formal answer: ASC 606, the revenue recognition standard that governs how SaaS companies recognize revenue today. Knowing the standard exists is the easy part. Applying it cleanly, every month, in a way that holds up under audit, is where most teams struggle.

This guide will walk you through ASC 606 applied to SaaS contracts, deferred revenue mechanics, journal entries, and what a clean financial close process looks like in practice.

Key Takeaways

- The standard isn't the hard part. Consistent execution across hundreds of contracts every close cycle is.

- SSP documentation is where bundled deal audits are won or lost — most teams underinvest until it's too late.

- Modification classification errors don't announce themselves. They compound quietly in the deferred revenue schedule until a restatement conversation starts.

- The deferred revenue roll-forward is only as reliable as the contract decisions made upstream.

- Audit readiness isn't a year-end project. The teams that handle due diligence cleanly built the infrastructure months before anyone asked for it.

What Is Revenue Recognition for SaaS?

Revenue recognition for SaaS is the accounting process that determines when and how much subscription revenue a company records in its financial statements. Under ASC 606, revenue is recognized when — and only when — performance obligations are satisfied: meaning the software service has been delivered to the customer for that period. Not when payment is received. Not when an invoice is issued.

Why Cash Received Is Not Earned Revenue

When a customer pays $12,000 upfront for a 12-month subscription, that cash hits the bank but is recorded as deferred revenue on the balance sheet. Only $1,000 gets released to the income statement each month as service is delivered. Conflating cash timing with earned revenue overstates income, violates GAAP, and is the kind of misstatement auditors flag.

ASC 606 vs. IFRS 15 — What SaaS Companies Need to Know

ASC 606 governs U.S. GAAP reporting; IFRS 15 governs international reporting. Both share the same five-step model and core recognition principle, making compliance logic largely portable for SaaS companies. The operational differences — primarily variable consideration constraint thresholds and disclosure requirements — are procedural but meaningful. Multinational teams need policies that explicitly address both frameworks.

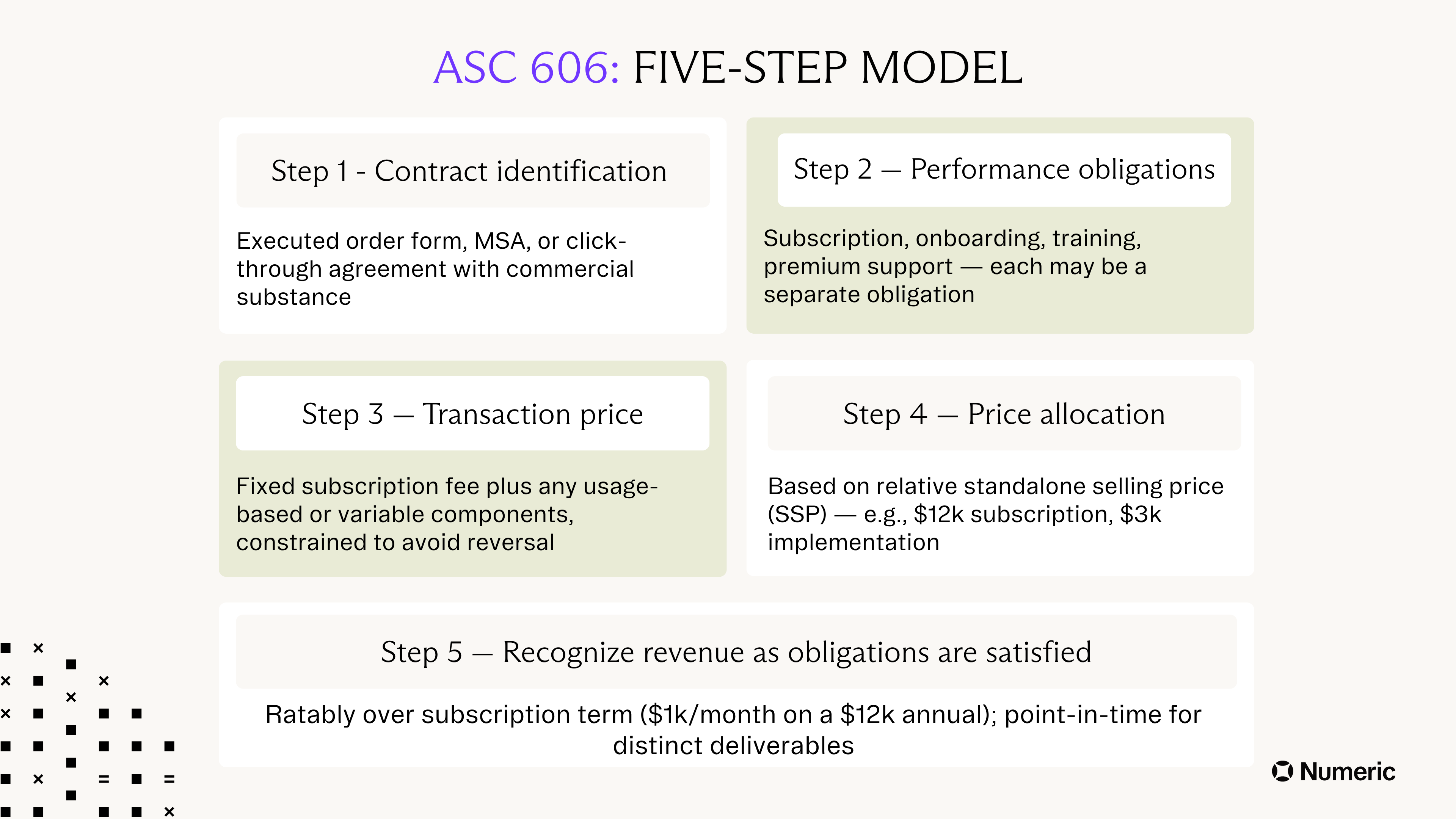

The ASC 606 Five-Step Model — Applied to SaaS Contracts

The five-step model is the standardized framework that governs SaaS revenue recognition. Every dollar of revenue a SaaS company records must pass through all five steps. And where those steps get applied — subscription terms, bundled contracts, mid-cycle modifications — is exactly where SaaS accounting gets complicated.

The model's numbered simplicity is misleading: Steps 2 and 4, in particular, involve judgment calls on performance obligation identification and standalone selling price (SSP) allocation, which are among the most frequently cited issues in SaaS audits.

Step 1 — Identifying the Contract

A contract exists under ASC 606 when both parties have approved it, identified the rights and payment terms, established commercial substance, and confirmed collection is probable. Verbal commitments, unsigned proposals, and letters of intent don't clear this threshold — a common audit risk at SaaS companies that begin revenue recognition before paperwork is finalized.

Step 2 — Identifying Distinct Performance Obligations

This is the step that most frequently breaks down in practice. A single contract bundling a SaaS subscription, onboarding, a training package, and premium support may represent four separate performance obligations — each with its own recognition timeline. Getting that separation wrong means your recognition schedules are off from day one — and that error sits in the schedule, growing harder to unwind with each subsequent record to report.

A good or service is distinct if the customer can benefit from it independently and it is separately identifiable from other contract promises. You can combine highly interdependent elements into one obligation, but you need documentation to support that decision.

Step 3 — Determining the Transaction Price

The transaction price is the total amount the company expects to receive, including both fixed and variable components.

For straightforward subscriptions, that's a clean number. For usage-based or discounted arrangements, the team has to estimate — and those estimates carry real audit risk.

You must estimate variable consideration — usage-based fees, volume discounts, refund provisions — using either the expected value method or the most likely amount method, and you can only include it to the extent that a significant revenue reversal is highly unlikely.

Step 4 — Allocating the Transaction Price Using SSP

Once you identify the obligations, you allocate the contract's total price based on each element's relative standalone selling price — what you would charge for that element sold independently.

This is where bundled deals get complicated. A single contract price has to be broken down across every obligation, and the split has to be defensible.

A bundled deal at $15,000 might allocate $12,000 to a subscription and $3,000 to implementation if those SSPs are observable from standalone transactions. When SSP isn't directly observable, teams use estimation methods — adjusted market assessment, expected cost plus margin, or the residual approach — each of which requires consistent application and written documentation to survive an audit.

Step 5 — Recognizing Revenue as Obligations Are Satisfied

You recognize SaaS subscription revenue ratably over the subscription period — $1,000 per month on a $12,000 annual contract — because the customer receives and consumes the benefit as service is delivered. One-time setup fees or implementation services may qualify for point-in-time recognition if they represent a distinct, fully transferred deliverable. If they don't meet the distinctness test, they fold into the subscription and are recognized ratably alongside it.

Working through the five-step model for every active contract produces one direct output: a deferred revenue balance that your team must actively manage, accurately classify, and release through journal entries each period. Teams looking to automate that workflow can see how revenue recognition automation handles the allocation and posting layer.

Deferred Revenue Accounting in SaaS — The Balance Sheet Liability You Can't Ignore

Deferred revenue in SaaS is a balance sheet liability representing cash collected for services not yet delivered. It is not revenue. That separation has to hold in your books every single month.

Under ASC 606, every dollar of deferred revenue must be released to the income statement on a schedule tied to performance obligation fulfillment. That makes the deferred revenue roll-forward one of the most consequential reconciliations in a SaaS close. It's also a direct downstream consequence of every contract decision made upstream in the order-to-cash process. It's also the one most likely to break when contract volume grows and the schedule lives in a spreadsheet.

Revenue Recognition Journal Entries — Step by Step

When a SaaS company collects a $12,000 annual subscription upfront, the full amount is recorded as deferred revenue. Each month, $1,000 moves from deferred revenue to the income statement as service is delivered.

Current vs. Long-Term Deferred Revenue — Getting the Classification Right

A two-year subscription paid upfront requires deferred revenue to be split: year one sits in current liabilities, year two in long-term liabilities. The classification has to be recalculated every time a contract is modified, renewed, or extended.

Misclassifying the long-term portion as current overstates near-term obligations and distorts working capital metrics that investors, lenders, and acquirers scrutinize closely. In a due diligence process, a deferred revenue misclassification tells auditors something broader about the quality of your financial controls.

Put Your Team on the Road to IPO

Contract Modifications — How to Handle Upgrades, Downgrades, and Mid-Term Changes

Contract modifications are among the most audit-sensitive transactions in SaaS revenue recognition because they require a classification decision before any accounting can occur. Get that classification wrong and everything downstream is off — the recognition schedule, the deferred revenue balance, and ultimately the numbers your auditors are reviewing.

Any approved change to a contract's scope or price — an upsell, a seat addition, a downgrade, an early renewal, an early termination — must be routed through a three-scenario framework. The revenue timing follows from that decision, and so does any restatement risk.

Treating a Modification as a New Separate Contract

When added services are distinct and priced at or above the standalone selling price, the modification is treated as an entirely new contract — independent of the original. Previously recognized revenue stays intact; the new contract starts its own recognition schedule from the modification date. This is the cleanest treatment operationally, but it requires robust SSP documentation asserting that the pricing reflects standalone value.

Prospective and Cumulative Catch-Up Adjustments

Prospective treatment applies when a modification adds distinct goods or services at a price below SSP — common in discounted expansion deals. Recognition schedule updates run forward without reopening historical periods. Choosing the wrong treatment means your recognized revenue is off from the modification date forward — and that error compounds every month until someone catches it.

Cumulative catch-up applies when the modification results in goods or services that are not distinct from what's already been partially delivered — most downgrades fall here. A catch-up requires recalculating recognized revenue as of the modification date and recording a one-time adjustment to bring the books current.

Both treatments require a documented modification memo covering the original contract terms, the change, the SSP analysis, and the accounting rationale. Auditors will ask for it.

Variable Consideration and Usage-Based Revenue — How to Estimate Without Overstating

Usage-based SaaS revenue — billed per API call, per active user, per GB processed, per transaction — falls under ASC 606's variable consideration rules. Variable consideration must be estimated and included in the transaction price only to the extent that a significant revenue reversal will not occur when the uncertainty resolves. That constraint forces finance teams to be deliberately conservative in early-period estimates for customers with unpredictable usage trajectories.

Expected Value vs. Most Likely Amount — How to Choose the Right Method

The expected value method calculates a probability-weighted average across all possible usage outcomes. It works best when a company has a large population of similar contracts with observable historical patterns. When that historical data doesn't exist — or when the range of outcomes is narrow — a different approach is needed.

The most likely amount method selects the single most probable outcome from a range of possibilities. It suits binary or narrow-range scenarios — for example, whether a customer will cross a volume threshold that triggers a discount tier. The method selected must be applied consistently within a contract type and documented to support audit review.

The Usage-Based Practical Expedient

ASC 606 provides a narrow expedient for certain output-based and sales-based fees. If variable consideration is allocated entirely to a single distinct performance obligation and the allocation terms are consistent with the overall allocation objective, the company can recognize revenue as usage occurs rather than relying on upfront estimates. This as-invoiced approach simplifies recognition for pure usage-based products. It only applies when specific criteria are met, and the election must be documented in the accounting policy.

Applying all of this across hundreds or thousands of active contracts, every close cycle, is where the technical accounting challenge becomes a daily operational one. The standard doesn't change — what changes is the volume of judgment calls your team has to execute correctly, every month. At that scale, the difference between an audit-ready close and an audit-exposed one isn't how well your team knows the standard. It's whether your processes can execute it reliably, without error accumulating in the background.

Building an ASC 606-Ready Close Process — Best Practices for SaaS Finance Teams

ASC 606 compliance is a continuous operational discipline. And SaaS companies that treat revenue recognition as a monthly checkbox are most likely to face restatements, audit adjustments, or investor scrutiny during due diligence. The gap lives in process — specifically, whether the infrastructure exists to apply that knowledge consistently at volume.

For teams navigating IPO readiness or first-time audits, infrastructure gaps tend to surface at the worst possible moment.

A best-practice close process for revenue recognition has several non-negotiable components:

- A centralized contract repository with signed agreements, order forms, modification records, and SSP analyses accessible to accounting and legal

- Recognition schedules maintained for every active contract, updated monthly to reflect modifications and renewals — not rebuilt from scratch when an auditor asks

- Documented SSP methodology for each product and service offering, updated annually or when pricing changes materially

- Consistent variable consideration policies with written frameworks for how estimates are developed, reviewed, and adjusted

- Clear separation of implementation and subscription revenue where performance obligations are distinct, with recognition policies documented and applied

- An audit trail for every journal entry, modification classification, and recognition schedule change — captured as it happens, not reconstructed before a fieldwork date

A purpose-built close checklist gives revenue recognition tasks the structure they need: assigned owners, clear dependencies, and review workflows that don't live in email or a generic project management tool. When your recognition schedule changes mid-month due to a contract modification, that update needs to be tied to the close task that owns it.

Teams that also use transaction monitors can go a step further, setting real-time alerts that flag when revenue entries fall outside expected patterns mid-month. Catching a misclassified modification in week two is a five-minute fix. Catching it at close is a fire drill.

When Manual Processes Start Costing You Close Time and Audit Credibility

Spreadsheet-based recognition schedules create compounding risk at scale. A single formula error in a deferred revenue waterfall can cascade across an entire contract cohort, producing misstated revenue figures that survive multiple close cycles before surfacing. And because the error is baked into the schedule, every subsequent month builds on it — by the time someone catches it, the restatement conversation has already started.

SaaS companies managing 200 to 300 active subscription contracts simultaneously often reach the point where manual processes can no longer maintain the accuracy, auditability, or speed required for reliable reporting.

The issue isn't just close time. When auditors request documentation for a contract modification from 14 months ago, "it's in a spreadsheet somewhere" is not a control. Understanding your exposure starts with knowing where your materiality thresholds sit — and whether your current process can defend them.

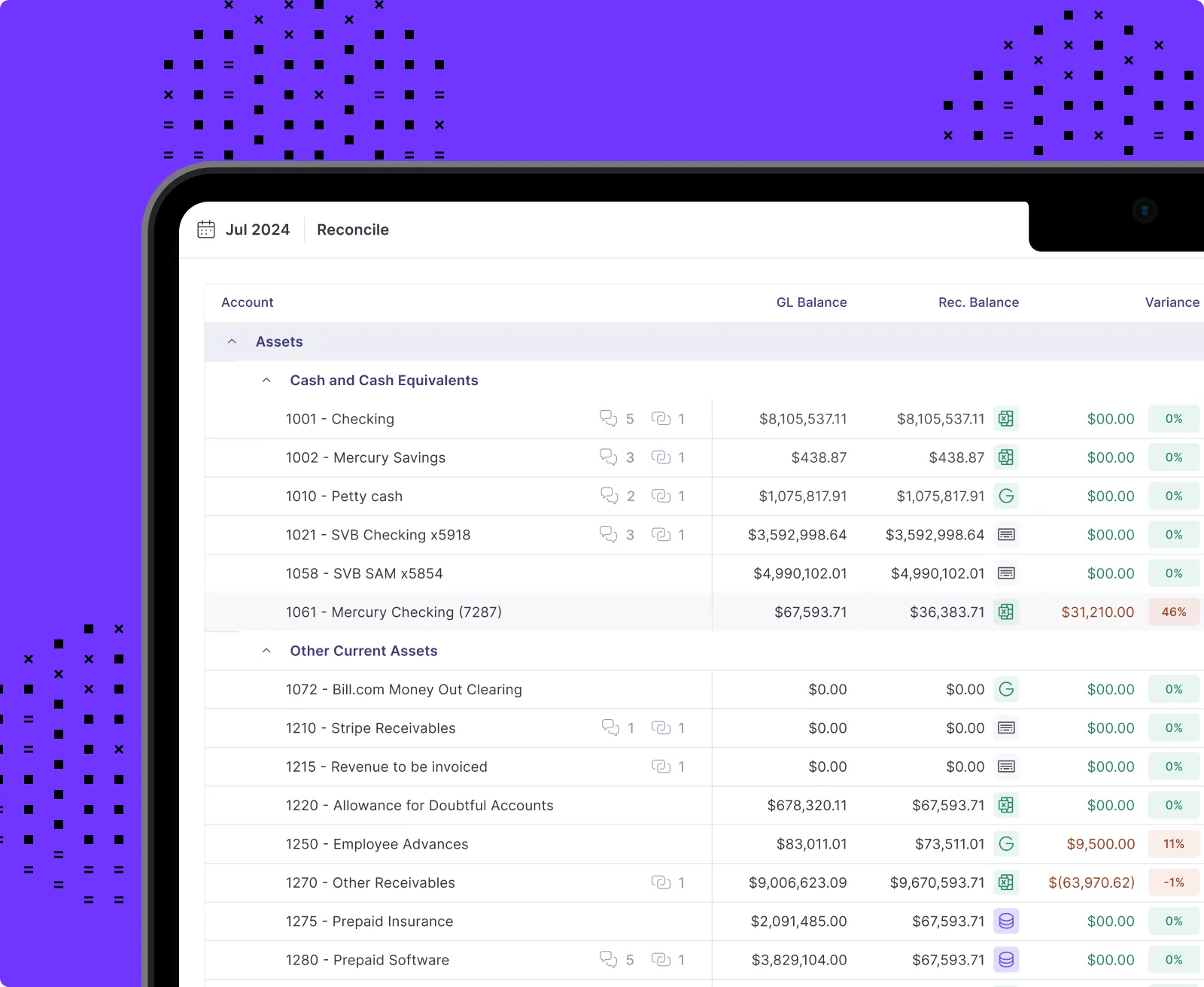

Reconciling Deferred Revenue Against the GL in Real Time

Once recognition schedules are running, the close team owns the tie-out between the deferred revenue subledger and the general ledger — and that is where errors from upstream classification decisions become visible.

Numeric's reconciliation platform pulls trial balance and subledger data directly from your ERP — NetSuite, Xero, QuickBooks Online, or Sage Intacct — and surfaces discrepancies at the transaction level, rather than waiting for a month-end mismatch to appear manually.

When a modification changes a contract's recognition schedule, the resulting deferred revenue movement is visible against the GL the same day — no manual tie-out across three systems. Every reconciliation, journal entry, and schedule change is captured on the platform as work happens.

For teams that need to explain revenue movement period over period, flux analysis makes that faster too. AI-drafted variance explanations for the revenue line mean less time writing commentary and more time reviewing the numbers underneath it. That matters most during audit prep and board reporting cycles, when finance teams are fielding questions from multiple directions, and the margin for error is lowest.

And when FP&A or leadership needs transaction-level detail, custom reporting surfaces that data without requiring a NetSuite expert or a one-off export.

Lean accounting teams that want the broader picture on how to build these close workflows at scale will find this breakdown on accounting operations useful alongside this guide.

ASC 606 Compliance Starts Before the Audit Clock Does

Revenue recognition quality is one of the first areas Big Four auditors, growth-stage investors, and M&A buyers examine. And the companies that enter those processes with defensible documentation, clean deferred revenue schedules, and consistent modification memos close faster and field fewer follow-up requests. The difference usually comes down to when they built the infrastructure — before the process started, or during it.

ASC 606 misapplication — particularly around multi-element arrangements, contract modifications, and deferred revenue misclassification — has disrupted funding rounds and delayed public market timelines.

"Newly public companies probably face the hardest version of compliance due to needing to build up that documentation from scratch. As companies scale, the burden really shifts from creation to maintenance. But if assembling evidence each season is super manual, then the audit season is always going to be a crisis regardless of company size."

— Jess Totoni, BDR at Numeric and former PwC auditor

The finance teams that avoid those outcomes aren't necessarily smarter about the standard. They built the infrastructure to execute it, at volume, with documentation.

The infrastructure gap shows up earliest in the close — in how modifications are tracked, how schedules are maintained, and how quickly the team can answer an auditor's question about a modification from three quarters back.

The best controllers use moments like audit prep not just to clean up the books, but to reposition finance as a strategic function — and a reliable revenue recognition process is foundational to that shift. That's where Numeric fits in: not as a substitute for technical accounting judgment, but as the operational layer that makes consistent execution possible at scale. For teams using LLMs, Numeric's MCP takes it further — letting you run recognition workflows, flag deferred revenue anomalies, and generate variance explanations all from one AI interface.

If your team is still managing revenue recognition in spreadsheets, book a demo to see how Numeric closes the gap — from deferred revenue tie-outs to a real-time audit trail that's ready when due diligence starts.

Frequently Asked Questions About Revenue Recognition for SaaS

Related Content

The Finance Engineer: Why Accountants Are the Best Builders in the Room

Why accountants, not engineers, are becoming the best builders on modern finance teams. Meet the Finance Engineer.

.png)

Numeric vs. Ledge: What's the Best Close Platform for Your Business?

A detailed comparison of Numeric and Ledge, two modern close management platforms, covering features, architecture, pricing, and a framework for choosing the right fit for your team.

.png)

What is Record to Report: Process, Steps, and Benefits

Learn how the Record to Report process works, from transaction capture to financial reporting. Discover steps, challenges, automation strategies, and best practices for modern accounting teams.